U.S. Department of Health and Human Services

Hospice Benefits and Utilization in the Large Employer Market

Beth Jackson, Teresa Gibson and Joline Staeheli

The MEDSTAT Group

March 2000

PDF Version: http://aspe.hhs.gov/daltcp/reports/empmkt.pdf (64 PDF pages)

This report was prepared under contract #100-97-0010 between the U.S. Department of Health and Human Services (HHS), Office of Disability, Aging and Long-Term Care Policy (DALTCP) and the Urban Institute. For additional information about the study, you may visit the DALTCP home page at http://aspe.hhs.gov/daltcp/home.shtml or contact the ASPE Project Officer, Jennie Harvell, at HHS/ASPE/DALTCP, Room 424E, H.H. Humphrey Building, 200 Independence Avenue, SW, Washington, DC 20201. Her e-mail address is: Jennie.Harvell@hhs.gov.

TABLE OF CONTENTS

- I. INTRODUCTION

- II. STRUCTURE AND IMPLEMENTATION OF HOSPICE BENEFITS IN COMMERCIAL PLANS

- A. Summary of Hospice Benefits

- B. Plan Discussions

- III. HOSPICE-RELATED UTILIZATION AND EXPENDITURES OF THE PRIVATELY INSURED

- A. Overview

- B. The MarketScan® Database

- C. Definition of Hospice Service Utilization

- D. Characteristics of Hospice Users

- E. Hospice Episode Construction Methodology

- F. Hospice Episodes Among the Commercially Insured

- G. Health Care Utilization for Commercially Insured Hospice Patients

- H. Health Care Expenditures for Commercially Insured Hospice Patients

- IV. DISCUSSION

- APPENDICES

- APPENDIX A: Example Memos and Sample Interview Schedule

- APPENDIX B: Additional Tables

- LIST OF FIGURES

- FIGURE III-1. Hospice Use Rates (per 1,000 covered lives) by Age and Sex, 1995

- FIGURE III-2. Illustration of Hospice Episode Construction Methodology

- FIGURE III-3. Mean Payments Pre, During and Post Hospice Episode

- FIGURE III-4. Pre, During and Post Hospice Episode Payments by Diagnosis for Individuals Receiving Hospice Services in 1995

- LIST OF TABLES

- TABLE II-1. Hospice Benefit Offered by Plan Type

- TABLE II-2. Characteristics of Hospice Benefit Package by Plan Type

- TABLE II-3. Services Covered Under the Hospice Benefit by Plan Type

- TABLE II-4. Characteristics of Plans Selected for Study

- TABLE III-1. Age and Sex Distribution of Insured Covered Lives Source

- TABLE III-2. Hospice Use by Age and Sex

- TABLE III-3. Rate (per 1,000) of Hospice Use by Employee Status and Relationship to Policy Holder

- TABLE III-4. Hospice Episode Utilization for Individuals Using Hospice Services in 1995

- TABLE III-5. Distribution of Hospice Episodes for Individuals Using Hospice Services in 1995

- TABLE III-6. Top 20 Diagnoses on Hospice Claims for Individuals Using Hospice Services in 1995

- TABLE III-7. Comparison of Hospice Care Diagnoses, United States and MarketScan®

- TABLE III-8. Sex by Terminal Diagnosis

- TABLE III-9. Region by Terminal Diagnosis

- TABLE III-10. Age by Terminal Diagnosis

- TABLE III-11. Length of Hospice Episode by Terminal Diagnosis

- TABLE III-12. Percent of Hospice Episodes Where Health Care Services Were Used Before, During and After the Hospice Episode

- TABLE III-13. Proportion of Episodes Associated with Use of Service Type and Terminal Diagnosis Before, During and After the Hospice Episode

- TABLE III-14. Pre, During and Post Hospice Episode Payments

- TABLE III-15. Pre, During and Post Episode Payments

- TABLE III-16. Pre, During and Post Hospice Episode Payments by Diagnosis for Individuals Receiving Hospice Services in 1995

- TABLE B-1. Distribution of Relation of Patient to Employee for Insured Covered Lives

- TABLE B-2. Distribution of Employee Status for Insured Covered Lives

- TABLE B-3. Regional Distribution of Insured Covered Lives

- TABLE B-4. Regional Distribution of Individuals Using Hospice Services in 1995

- TABLE B-5. Rate of Hospice Service Use by Region for Individuals Using Hospice Services in 1995

- TABLE B-6. Distribution of Relation of Patient to Employee for Individuals Using Hospice Services in 1995

- TABLE B-7. Primary Diagnosis by Relationship of Patient to Employee Category for Hospice Episodes for Individuals Using Hospice Services in 1995

- TABLE B-8. Payments for Users of Inpatient or Outpatient Services Pre, During and Post Hospice Episode by Diagnosis for Individuals Receiving Hospice Services in 1995

EXECUTIVE SUMMARY

This study, sponsored by the Office of the Assistant Secretary for Planning and Evaluation (ASPE), U.S. Department of Health and Human Services, is part of a larger project exploring the use of hospice benefits and services provided by the Medicare program and to those who are privately insured. The MEDSTAT Group's contribution to the larger study is an examination of hospice benefits in commercial plans and the use of hospice benefits by persons commercially insured. In particular, this report focuses on hospice benefits in plans offered by large employers in the U.S. and the utilization of hospice benefits by the employees of these large companies, their dependents, and in some cases early retirees. We draw upon MEDSTAT's proprietary MarketScan® database for all of the analyses in this study. MarketScan includes about 70 employers and 200 insurance carriers/claims administrators. It is a database that represents the health care experience of about four million privately insured individuals annually.

Three complementary approaches to the study of commercially-insured hospice were taken in this study:

- An analysis of hospice benefits offered by large employers through examination of their Summary Plan Description (SPDs) booklets;

- Discussions with selected large employers about their hospice benefits; and

- A quantitative analysis of hospice use and expenditures of persons commercially insured.

First, we examined the nature of the hospice benefits offered by some of the large employers represented in MarketScan through a content analysis of their Summary Plan Description booklets (SPDs). The plans were classified according to whether they offered a hospice benefit, the conditions under which hospice benefits are provided (precertification, waiver of curative treatments), and applicable deductibles, coinsurance and limits. In addition, we examined the services that are covered under the plan's hospice benefit. Since the amount of information available in the SPDs regarding the hospice benefit tended to be scant, we augmented the SPD content analysis with telephone discussions of a subset of employers in the MarketScan database who offered a hospice benefit. The purpose of the interview was to collect detailed information on the rationale behind the current structure of the plan's hospice benefit, information on changes in the hospice benefit over time, and how employers/plans managed the benefit once accessed. The third component of this study is a quantitative analysis of hospice use and expenditures among the commercially insured using the MarketScan data.

Our analysis of the commercial plans included in the MarketScan database show that hospice is a commonly offered benefit that appears in a wide variety of configurations across employers and plans. The vast majority (88 percent) of the health plans examined in this study offered a hospice benefit. And condition eligibility on precertification of terminal illness by a physician. However, only half the plans requiring precertification of terminal illness specified a definition of terminal illness in the SPD, all defining terminal illness as 6 months or less to live.

There was a great deal of variation in the cost sharing (coinsurance and deductibles) provisions of the hospice benefit, lifetime limits (maximum hospice days and dollars) and coverage of hospice-related services. Most plans did not impose cost sharing requirements on the hospice benefit. For the plans that required cost sharing from the employee and dependents, coinsurance and deductible levels covered a wide range of dollar amounts, some tying cost sharing amounts to salary levels. A few PPO and POS plans increased the cost-sharing amount if the individual received services from an out of network provider. Lifetime maximum day and dollar limits were infrequently and inconsistently imposed.

The percentage of plans explicitly mentioning coverage of hospice services across settings of care (inpatient hospital, hospice facility and at home) also varied considerably. PPOs (in contrast to POS and Indemnity plans) identified the fewest number of covered services and settings in which hospice services are covered. Thirty-seven percent of plans imposed dollar caps and 11 percent set day limits.

Telephone discussions with eight of the plans shed more light on the amount of flexibility and discretion exercised by employers and plans in the administration and implementation of the hospice benefit. While the plan designs appear to be rigid, many of the employers and plans revealed during the discussions that hospice provisions were often perceived as guidelines and typically were not stringently applied. If a specific benefit ran out, the employer or plan often extended or renewed the needed benefit. Employers and plans consistently reported that flexibility in these instances was "the right thing to do", and at the same time acknowledged that it was possible to exercise such flexibility because the demand for hospice is so low in the commercially insured population.

Three general approaches to the design and administration of the hospice benefit were revealed as a result of our discussions with employers:

- Medicare-like Model;

- Comprehensive Model; and

- Unbundled Model.

Plans adopting the Medicare-like Model (2 out of the 9 plans interviewed) structured their hospice benefit based upon the Medicare program's hospice benefit. These plans impose similar benefit periods and eligibility requirements as the Medicare program and require a waiver of curative treatments when hospice care commences. Half of the plans interviewed adopted a different approach, the Comprehensive Model, significantly deviating from the Medicare-like Model. Notably, suspension of curative treatments is not required while a patient undergoes hospice treatment under this model. Curative and palliative treatments can occur simultaneously. Coverage of both types of care is seen as humanitarian and caring by the employers, especially under circumstances often perceived as untimely and tragic for the population served. Finally, the Unbundled Model provides hospice service coverage for care unique to hospice, although the hospice benefit is subject to lower lifetime limits than the other models. All non-hospice care is provided under other plan provisions (e.g., prescription drugs are paid through the outpatient prescription drug plan, home health through the medical plan, etc.). Case managers are responsible for coordination of the entire spectrum of care for the terminally ill individual under the unbundled mode.

The various model types adopted by commercial plans can be instructive to those in government-sponsored programs, commercial plans and research organizations seeking new approaches to end of life care and benefit configurations for delivery of end of life services. Innovative approaches to end of life care (vis-à-vis the Medicare-like Model) have been uncovered in this exploratory study including the case management of hospice services, combinations of palliative care and curative treatment, and integration of hospice into a variety of managed care programs. Further study of how commercial plans are evolving their hospice benefit, especially their successes and lessons learned, may provide useful information to developers of programs to serve terminally ill individuals enrolled in all types of health care plans including Medicare and Medicaid.

Two other issues frequently associated with hospice services, fraud and abuse and cost effectiveness were briefly explored during the discussions. Even in light of the fact that hospice service fraud and abuse have been a major concern for government-sponsored hospice programs, employers expressed relatively little concern about the potential for fraud and abuse of the hospice benefit. Employers cited the extremely low levels of utilization of the hospice benefit, due to the relatively healthy population that they insure, as the main reason for their lack of concern. Where concerns were expressed, the use of dollar and day caps or requiring case management were cited as measures to mitigate the risk of abuse of the hospice benefit and/or a means for providing care more tailored to the needs of the dying person and his/her family.

Analysis of the expenditures and utilization patterns of hospice service users in the 1995 MarketScan database revealed, not surprisingly, that hospice services are used infrequently in this younger, employed population. Less than one person in 1,000 (0.43 persons) used hospice services in 1995. Also not surprising, hospice use rates were associated with age. While use rates were relatively low for enrollees 0 to 35 years of age (under .20 per 1,000 covered lives), hospice use rates rose considerably in the older age categories.

Hospice episodes of care were found to be brief, with a mean episode length of 21 days and a median length of 1 day per episode. Over half (59 percent) of the episodes consisted of 1 day of hospice care. Whether one-day episodes reflect the reluctance of physicians and their patients to access hospice or some other phenomenon, e.g., an artifact of how claims are filed, was beyond the scope of this investigation, but would be fertile ground for further study. Medicare hospice episodes are also short in duration relative to the length of the chronic illnesses associated with them -- but not as short as those of the commercially insured. The fact that the commercially insured population using hospice is younger, on average, than the Medicare hospice population, and thus perhaps even less inclined to accept their imminent mortality may be part of the explanation.

Although commercially-insured hospice service users in this study are small in number, they are a relatively diverse group of individuals ranging in age from 0 to 88 years with a wide variety of terminal conditions including rare congenital diseases and common cancers. From a diagnostic standpoint, these individuals generally resemble hospice service users in the US. However, commercially-insured hospice users had a higher percentage of AIDS diagnoses and a lower percentage of circulatory disorders and heart disease conditions than the entire population.

The diversity of commercial hospice service users is further noted by differences in cost and service utilization across terminal diagnosis categories. Episode use and cost patterns for individuals with all cancers (breast, lung and other) appeared to be relatively similar, but individuals with "Other" conditions (non-AIDS, non-cancer) tended to have shorter episodes, lower payments, younger ages and a lower use of home health services than those with cancer. Individuals with AIDS tended to be younger, have longer episodes, higher payments and used home health services more often than those with cancer.

Mean payments per hospice episode were relatively low, $2,951 for hospice services and a similar amount for non-hospice medical services ($3,114). Spreading the cost across the entire insured population, hospice service payments per covered life were nominal, around $1.18 per covered life per year. On average, total (hospice and non-hospice) payments for the entire time period covering the 60 day pre-episode period, the hospice episode and the 60 day post-episode period were about $20,000, around $14.50 per covered life per year for all care.

Perhaps the most striking finding of this study is the degree to which commercial plans deviate from the Medicare hospice model, both in terms of the nature of the population served (age) and in benefits administration. A minority of plans adhere to the government model -- described as rule-bound, proscriptive. Most commercial plans seem to administer their hospice benefits with a fair modicum of flexibility, accommodating the needs and desires of patients and families. It is also clear, however, that commercial plans can afford this flexibility given the low demand for the service in their covered populations. While we did not examine hospice in the non-fee-for-service environment, we did detect a small but potentially significant groundswell of plans, PPOs in particular, opting to carve out and/or unbundle their hospice benefit and link it to case management. These unbundled, carved-out and case-managed models are ripe for further investigation as the federal government explores options for its Medicare hospice benefit and as commercial plans seek to restructure their hospice benefits so they are appropriate and cost-effective for their covered populations.

I. INTRODUCTION

This study, sponsored by the Office of the Assistant Secretary for Planning and Evaluation (ASPE), U.S. Department of Health and Human Services, is part of a larger project exploring the use of hospice benefits and services provided by the Medicare program and to those who are privately insured. The MEDSTAT Group's contribution to the larger study is an examination of hospice benefits in commercial plans and the use of hospice benefits by persons commercially insured. In particular, this report focuses on hospice benefits in plans offered by large employers in the U.S. and the utilization of hospice benefits by the employees of these large companies, their dependents, and in some cases early retirees. We draw upon MEDSTAT's proprietary MarketScan® database for all of the analyses in this study. MarketScan includes about 70 employers and 200 insurance carriers/claims administrators. It is a database that represents the health care experience of about four million privately insured individuals annually. MarketScan links paid claims and encounter data to detailed patient information, across employer sites, types of providers, and over time. More than 500 million claim records are available in the MarketScan database.

Three complementary approaches to the study of commercially-insured hospice were taken in this study, all in one way or another involving the MarketScan database. First, we examined the nature of the hospice benefits offered by some of the large employers represented in MarketScan through a content analysis of their Summary Plan Description booklets (SPDs). The plans were classified according to whether they offered a hospice benefit, the conditions under which hospice benefits are provided (precertification, waiver of curative treatments), and applicable deductibles, coinsurance and limits. In addition, we examined the services that are covered under the plan's hospice benefit.

Since the amount of information available in the SPDs regarding the hospice benefit tended to be scant, we augmented the SPD content analysis with telephone discussions with a subset of employers in the MarketScan database who offered a hospice benefit. The purpose of the discussion was to collect detailed information on the rationale behind the current structure of the plan's hospice benefit, information on changes in the hospice benefit over time, and how employers/plans managed the benefit once accessed. Section II reports findings related to the structure and management of hospice benefits in the commercial sector, and includes results of our analysis of the SPDs and our discussions with employers.

The third component of this study is a quantitative analysis of hospice use and expenditures among the commercially insured using the MarketScan data. In Section III we present information on the demographic characteristics of persons using hospice care as a commercial insurance benefit, the average lengths of hospice episodes for this population, diagnoses associated with episodes, and the types and amounts of hospice and non-hospice services utilized before, during and following (if any) the hospice episode. Section IV presents a summary and discussion of the findings of the study in toto.

II. STRUCTURE AND IMPLEMENTATION OF HOSPICE BENEFITS IN COMMERCIAL PLANS

A. Summary of Hospice Benefits as Described in Summary Plan Descriptions

Our initial foray into an examination of hospice benefits among commercial health insurance plans was an audit of selected Summary Plan Descriptions (SPDs) of the health plans that are included as part of MEDSTAT's MarketScan® Database. This database consists of linked paid claims1 to detailed patient information, across employer sites, types of providers, and over time. In addition, the employers participating in MarketScan routinely provide to MEDSTAT the SPDs for the health plans that they offer. This audit activity was undertaken to garner as much information as possible from the SPDs about hospice benefits in commercial plans.

1. Methodology

MEDSTAT has SPDs for approximately 60 percent of the covered lives in the MarketScan database. However, a review of the entire collection of SPDs was prohibitive given the resource constraints of this project. Our target sample size was approximately 50 fee-for-service plans2, and we actually reviewed 52 SPDs. Our sample was purposive in that we wanted to insure that the majority of plans we reviewed would offer a hospice benefit, and among those that did, we wanted to include the ones with the most experience with hospice use (defined as number of hospice claims) among their insured population. Thus, our sample includes the 11 plans (representing 10 employers) with the highest hospice use rates, operationalized as greater than 10 hospice users per 1,000 covered lives. The sample was devised to also include the plans with the highest number of covered lives. As such, twelve plans with more than 20,000 covered lives and representing 9 employers also underwent SPD review. While these plans may not necessarily have had the highest rates of hospice use, they were included because they had a greater chance of having experience with hospice use given the sheer number of the lives they covered. We also included the largest plans since they tend to be trendsetters in the industry, and we were interested in what hospice benefits they offer. We also felt that it was important to include in the sample plans that had neither very large numbers of covered lives nor high rates of hospice use. As a consequence, the SPD review sample includes an additional 12 plans in this category. And finally, because we were interested in examining some basic differences between plans that did and did not offer a hospice benefit or plans that did not have any experience with the hospice benefit despite offering one, we also included those without any hospice experience (claims) -- another 17 plans.

Following an initial review of the sampled SPDs, an SPD database was created detailing the hospice benefits offered by each plan, as well as the hospice benefit-related conditions imposed by the plan, e.g., deductibles, co-payments, lifetime limits, etc. In addition, we recorded whether and how an SPD described the hospice benefit/services, whether or not precertification was necessary to access the benefit, and whether the SPD specified an operational definition of the term "terminal illness" (the condition to which hospice benefits are targeted). Following the development of the database elements, each SPD was reviewed a second time, coded on all relevant data elements, and entered into the database.

2. Results

Of the 52 SPDs selected for analysis, hospice was identified as a covered benefit in 46. Table II-1 depicts the distribution of plans according to whether they offered a hospice benefit, by plan type: Indemnity, Point of Service (POS) or Preferred Provider Organization (PPO). A very high proportion of each plan type (84.4 percent to 100 percent) offered the benefit.

The remaining results in this section are based on the 46 SPDs that offered an explicitly specified hospice benefit. They represent 19 large employers. The data were collected in the early winter of 1998, but since plans do not typically update SPDs annually, the SPDs available ranged from 1986 to 1996.

The percentages in Table II-2 represent the proportion of plan types with certain hospice benefit-related criteria. As this table shows, the vast majority of plans provided a definition of hospice and required precertification of being terminally ill by a physician. All SPDs providing a description of the hospice benefit identified the terminally ill as its target group. But only half of the plans provided an operational definition of the term "terminally ill". In all cases where a definition was provided, "terminally ill" was defined as 6 months or less to live.

Generally speaking a minority of plans, ranging from one-fifth to slightly less than half of the plans in each plan category, impose deductibles or coinsurance on the hospice benefit. The major exception is for out-of-network utilization for the POS and PPO plans, where 100 percent and 50 percent of the plans, respectively, require coinsurance. Deductibles for hospice services ranged from $0 to $2,000 (mean = $356) for individual coverage and from $0 to $4,000 (mean = $793) for family coverage. A couple of plans varied the deductible amount based on the employee's salary. It is interesting to note that the proportion of plans applying a deductible to hospice benefits (37 percent) is fairly comparable to the proportion requiring deductibles for skilled nursing services or services provided in an extended care facility (39.1 percent) and for home health services (45.7 percent). Of those that require coinsurance for hospice benefits (39.1 percent), approximately 78 percent require a 20 percent coinsurance payment and 22 percent specify a 10 percent coinsurance payment. For those plans that permit access to out-of-network providers, all require coinsurance, ranging from 15 percent to 50 percent.

The majority of plans do not impose a lifetime day or dollar limit. However, of the 10.9 percent that stipulate a day limit 80 percent have a 180-day limit and 20 percent (representing 1 plan) have a 270-day limit. Dollar limits are somewhat more common and exist in 37 percent of plans. Dollar limits range from $5,000 to $10,000; 70 percent of plans with a dollar limit set the limit at $5,000.

Table II-3 displays the proportion of plans (by plan type) that specify in their SPD that they offer a given service under the hospice benefit. The proportion that report offering a benefit, however, should be interpreted with caution; in many instances a plan neither mentioned the services as included nor excluded under their hospice benefit. If the service is not specified as included in the benefit, it is not safe to conclude that it is not offered. Also, the same service might be provided as non-hospice benefits under the same plan. As will be discussed later in this report, a great deal of latitude in service provision is afforded under the hospice benefit by both employers and plans. Determinations are often made on a case-by-case basis, a practice which employers sanction since it promotes good will and is not costly given the low level of utilization among this group of relatively healthy insureds (i.e., employees and their dependents).

The data in Table II-3 indicate that the indemnity and POS plans offer the widest variety of hospice services. For both of these plan types, a variety of venues for the provision of hospice care seems to prevail -- in the hospital, in a hospice facility, and at home. A smaller proportion of plans will reimburse for hospice services provided in an extended care or skilled nursing facility. Counseling, both for the terminally ill individual and for family members, is also a benefit that is specified in the majority of indemnity and POS SPDs. Other services such as respite care, homemaker, home health aide, equipment, etc. are less likely to be indicated. The low percentage of PPOs offering hospice services other than in- home hospice care is perplexing.

B. Plan Discussions

In this section we report on information garnered from discussions with a small, and not necessarily representative, subset of large employers who offer a hospice benefit as part of their medical insurance coverage. The methods section that follows describes the research team's approach to identifying sample interviewees and the content and structure of the discussions. The methods section is followed by several sections describing the structure of the hospice benefit in the commercial world, as represented by the plans we examined in depth. Since most plans are designed independently, it is not surprising that we uncovered multiple approaches to hospice benefit design and management. Thus, the later parts of this section describe three hospice benefit models uncovered among the subset of plans we studied, and include case studies of each of the models.

1. Methodology

a. Sample Selection. Potential employers for the discussions were identified using the MEDSTAT MarketScan® Database from 1995. Initially, we had intended to choose plans based on utilization rates using hospice claims (inpatient plus outpatient) per 1,000 covered lives as an indicator. This approach for sample identification was abandoned, however, since several of the plans fell into the high-rate category despite the fact that there were only a few persons accessing hospice benefits -- due to the fact that the number of lives covered by the plan was relatively small, i.e. small denominator.

Having abandoned plan selection based on hospice use rates, volume of hospice claims became the key indicator in identifying employers/plans for discussion. Seven of the nine initially chosen were selected because they represented plans with the greatest number of beneficiaries using the hospice benefit. Two plans with non-existent hospice use (despite offering a hospice benefit) were also chosen for comparison purposes. When two of the initially selected employers, one representing a plan with no hospice claims in 1995, declined to participate in the study, two additional plans were substituted bringing the total sample for discussion to nine. The final sample includes eight plans with a "high" volume of hospice users, and one plan with no hospice experience in 1995.

Table II-4 enumerates each of the employer-plan pairs selected for discussion (with identities masked for confidentiality). For each employer-plan pair, information on the plan type, the number of lives covered by the plan in 1995, and an unduplicated count of persons utilizing the hospice benefit in 1995 is provided. In this exhibit, plan type refers to the different service or payment arrangements under which health care services are provided -- Point of Service (POS), Preferred Provider Organization (PPO) or Indemnity coverage. The number of covered lives indicates the number of subscribers enrolled in the specified plan, and includes employees, their dependents, and some early retirees. The number of persons accessing the benefit refers to the number of beneficiaries with inpatient or outpatient hospice claims to the plan during 1995, and represents the volume of hospice use in the plan. The last column in Table II-4, labeled "Hospice Model", reflects the underlying structure and approach to managing the hospice benefit that the plan had adopted. These models are discussed in depth toward the end of this section.

Our final discussion sample as depicted in Table II-4 includes six indemnity plans, two POS plans and one PPO. The sample's number of covered lives ranges from a low of nearly 7,000 (Plan H) to a high of nearly 214,000 (Plan C). Although all but one of these plans were selected because they represent commercial plans with the most experience with hospice use in MarketScan, the number of beneficiaries accessing hospice in each of these plans is relatively small. In reality, only between 19 and 104 beneficiaries in each of these "high volume" hospice plans had used a hospice benefit in 1995. Such low volume among the commercially insured is due to one major characteristic of these populations: they are predominantly employees and their dependents, therefore relatively young and healthy, and thus less likely to need endof-life care and hospice services.

b. Discussion Protocol. A semi-structured discussion protocol was designed after a close review of Summary Plan Descriptions (SPDs) of the nine plans selected. Some SPDs provided sparse information on such aspects of the hospice benefit as types of services offered, how exclusions or lifetime caps functioned, and the general history and rationale behind the benefit. Consequently, part of the discussion protocol was designed to collect comparable information about the hospice benefit from this subset of plans and to augment the information provided in the SPDs. In order to secure information unavailable in the SPDs, additional questions about the history of the plan's hospice benefit, the rationale for how hospice benefits were structured (limits, caps, carve-outs, etc.), and how employees/dependents access hospice benefits were also built into the discussion schedule. During the discussion employer representatives were asked:

- When and why the current hospice benefit had been offered;

- Whether any changes had occurred in the benefit since it was adopted;

- Rationale behind the current structure of the plan's hospice benefit (i.e., limitations, caps, and offered/excluded services);

- Whether other benefits are reduced when an enrollee elects hospice coverage;

- What definitions of hospice or terminal illness are used for precertification purposes;

- How beneficiaries decide to enter hospice care (i.e., role of the physician, case manager, hospice division, or benefits department in implementing and encouraging hospice enrollment); and

- How the selected plan's hospice benefit differs from the other plans offered by the employer.

Since there was considerable variation in the hospice benefit as described by the SPDs and in the detail the SPDs provided about the hospice benefit, the discussion protocol was tailored to each employer/plan pair. An example of a tailored discussion schedule may be found in Appendix A, at the end of this report.

c. Contacting Employers. A letter explaining the project and its purpose was sent to the MEDSTAT client manager of each employer selected for discussion (See Appendix A). The client manager then contacted the employer, explained the study, and recruited the employer for study participation. Once this initial contact had occurred and the employer had consented to the discussion, a packet of information including an introductory letter (See Appendix A), a summary of the hospice benefit offered by the plan (excerpted from the SPD), a copy of the plan SPD used for summarizing the plan's hospice benefit, and a series of questions specifically tailored to the plan was sent to the employer representative identified by the MEDSTAT client manager. A follow-up call was then made by the research team to schedule a telephone discussion.

Nearly all the discussions were conducted with persons working as analysts, directors, or managers in the corporate benefits, insurance operations, research and development, or health strategies departments for the employer. However, two employers decided that the person most familiar with their hospice benefit was, in one case, a director of medical case management within the plan administration, and in the second case, the employer's account representative within the plan. We were successful in securing discussions with both of these individuals.

Conference calls with each interviewee were arranged and conducted over the course of three weeks between March 30, 1998 and April 17, 1998. Most discussions lasted approximately 30 minutes. In two instances interviewees were unavailable for a conference call, and chose to provide written responses to the discussion questions. A short follow-up call was conducted after receiving the written responses in order to pursue any additional information that the research team felt necessary to complete a description of the hospice benefit in the plan of interest.

2. Results

All the plans examined emphasized a definition of hospice as palliative care provided in several different locations (freestanding hospice, at home, hospital, and nursing home) and augmented by supportive counseling. Services typically associated with every plan's hospice benefit include: home health care, various speech, physical, or respiratory therapies, pharmaceuticals, durable equipment, medical supplies, individual counseling, social worker services, and some inpatient care for pain management. Terminal illness, confirmed by physician diagnosis, was necessary for a patient's entry into each plan's hospice benefit. With only one exception, terminal illness was defined as having less than 6 months to live. The exception precertified hospice enrollment only after a prognosis of 30 days left to live.

Only one plan had significantly changed its hospice benefit structure since its initial inception; this happened to be the plan that had no hospice utilization in 1995. The benefit was modified from covering inpatient hospice only, to covering of all types of hospice arrangements (i.e. home care, hospice facility care, and nursing home care). According to the representative interviewed, hospice utilization has increased since the change.

A cursory review of SPDs creates the misperception that the structure of the hospice benefit in commercial plans is quite disparate. For example, while some SPDs specify strictly limited respite care or provided none at all, others were less definitive. Another service that seemingly varied widely was the type and amount of counseling available to the patient and family members. However, we learned during our discussion that adherence to SPD restrictions and limits is not rigorous, particularly in cases where an employee or dependent needs a service not typically covered or after exceeding the financial limit of the plan.

None of the representatives expressed concern about abuse of their hospice benefit as currently constructed. One representative suggested that low utilization rates and the fact that home hospice care is historically less expensive than life-saving measures performed in the hospital, there is no need for measures promoting cost-containment. Several representatives did indicate that the potential for escalating costs motivated the implementation of lifetime caps and the restrictions on services. One of the interviewees employed by a health plan reported some concern over hospice agency exploitation of the hospice benefit. To prevent this, the plan relied on case managers to authorize the services and monitor billings for hospice care.

The sample for this investigation was purposive and as such, no claim of generalizability to all commercial plans offering a hospice benefit can be made. Nevertheless, as a result of our analyses of the data collected in the qualitative discussions, three relatively distinct models of commercial hospice benefits emerged:

- Medicare-like Model

- Comprehensive Model

- Unbundled Model

Since only nine employer/plan pairs participated in the in-depth discussions and since it is only by closely examining how plans administer the hospice benefit, no attempt has been made to apply the above classification to all of the plans included in the MarketScan database. Moreover, the interviewed employers/plans were selected non-randomly, and thus we cannot generalize the distribution of the models to all the health plans in the MarketScan database. Below we describe the common features of each of the hospice model types we uncovered. We also provide an example of each by presenting one case study for each of the paradigms.

a. The Medicare-like Model. Plans with hospice benefits structured according to a Medicare template have several characteristic features. First, to obtain precertification, the patient must submit a signed waiver of the right to curative treatment. Second, after the beneficiary opts for hospice s/he is enrolled in an initial ninety-day period. At the end of this period, s/he may opt for another ninety days of hospice care or revert back to non-hospice status. A final period (thirty days) of hospice eligibility is allowed if the beneficiary so chooses.3 Third, hospice benefits designed to model Medicare are organized according to levels and intensity of care needed: routine, continuous or crisis care, inpatient (including nursing home) or respite care. The referring physician decides when the patient is eligible for different levels of care, and the care is provided or coordinated by a hospice agency.

Two of the plans we examined (Employer Plan F and Employer Plan G) modeled their hospice benefits after the Medicare hospice benefit (See Table II-4). Both employed the defined periods of care as described above. In addition to the day limit, one of these plans relied upon the dollar cap set by Medicare (currently $14,394). For these plans, covered hospice services were rigorously outlined in the plan booklets, though these included all of the services generally offered by hospice agencies -- with the notable exception of Plan F where homemaker/custodial care was not covered. Upon probing, however, the representative from Employer Plan F indicated that if such care were included within the per-diem rate paid to the hospice agency, custodial care would be covered by the hospice benefit.4

| Employer Plan FAn Example of the Medicare-like Model |

| Employer Plan F's indemnity plan embodies the three major features of the Medicare-like Model: specified enrollment periods, waiver of curative therapies, and graduated levels of care prescribed by a physician. This plan reported a very high percentage of hospice users who were also eligible for Medicare (presumably retirees). The representative felt that structuring the benefit by closely adhering to the Medicare-like Model would enhance patient satisfaction, since the plan would supplement Medicare coverage. Employer F does not adhere to the Medicare defined cap on hospice care, but instead limits care according to a maximum number of days of hospice care (i.e. a total of seven months of care.) A one million dollar total lifetime limit including all care is also in effect, though the representative indicated that to her knowledge there has never been a case approaching either the maximum hospice day limit or the 1 million dollar limit. Employer F stressed that although the rules appear rigid, they are treated more as guidelines. Recently, Employer F shifted many of its plans from indemnity coverage to PPOs, simultaneously creating a hospice division separate from any plan or network. In essence, the hospice benefit is now a carved-out service, but the day limit on hospice care is still enforced. Under the current structure the patient must still be referred by a physician, but the patient also must attend a presentation by the plan's hospice division. |

Both of these plans demand a signed waiver suspending a patient's access to curative therapies while enrolled in hospice. This waiver does not suspend care for conditions unrelated to the terminal illness. For example, if a patient were to fracture a bone while enrolled in hospice s/he would certainly have access to curative treatment for this condition. Each of these plans stressed that the purpose of the waiver was to ensure that patients fully understood the palliative focus of hospice. Plan policy varied on whether curative treatment could be immediately resumed if a patient decided to leave hospice, though both plans indicated that such a request would be subject to a case by case review. This model places primary importance on the physician's discretion and guidance of the treatment protocol.

b. The Comprehensive Model. The main feature of the comprehensive hospice model includes generous hospice coverage with minimum restrictions placed on hospice providers by the plan, and no dollar or day limits on utilization. Unlike plans adhering to the Medicare-like Model, plans under this model do not require a suspension of curative modalities upon election of the hospice benefit.

Four of the employers interviewed in the study had plans that can be described as fitting the Comprehensive Model (Employer Plans B, D, E, and H). In this model, a physician must certify that the beneficiary is terminally ill. Once certified, benefits flow as determined by need and as assessed by a hospice provider. Even if a certain service were not specified as included in the hospice benefit as described in the SPD, the plan would cover it as long as the hospice agency determined it was necessary and it was included within the per diem rate. Although we have included it under the Comprehensive Model, the PPO plan (Employer Plan B) did encourage beneficiaries to use network providers, only paying 80 percent of the charges of an out-of-network hospice provider. Plan B's representative suggested that since their network included ample hospice providers the co-pay provision for out-of-network providers was not restrictive and actually was implemented to protect patients from less than adequate providers.

| Employer Plan HAn Example of the Comprehensive Model |

| By offering comprehensive hospice coverage without a dollar or day limit, Employer H is an ideal representative of the comprehensive model. Employer H's benefit designers opted for a per-diem rate approach -- one they see as maximizing provider and patient autonomy and consequently enhancing the patient-provider relationship. Suspension of curative treatments relating to the terminal illness was not even considered by Employer H, unlike the Medicare-like Model where patients must forego coverage for curative treatments. Though Plan H's SPD indicated a $7000 lifetime hospice limit, the limit would be waived if a beneficiary happened to exceed it. There had been much discussion internal to the company where those in favor of the limit sought to protect the plan from excess utilization, while those advocating removal of the limit were concerned about restricting necessary patient care as well as the potential liability of enforcing a relatively low limit. It is interesting to note that despite the dollar cap, Employer H reported that rarely did a patient even approach the maximum. Although there was more concern about the potential cost of the benefit when it was first offered, Employer H's experience over the years has shown that home-hospice care has proven to be very cost-effective. There is no longer any concern about potentially exorbitant outlays related to the hospice benefit. In the words of Employer H's representative, offering a hospice benefit is "both ethically and financially the right thing to do. While it lets people choose where and how they want to die, it saves the plan money. It [hospice] is a win-win situation." |

c. The Unbundled Model. Plans characterized by the third paradigm, the Unbundled Model, seek to maximize their subscribers' benefits and to control the cost of services by unbundling pre-packaged hospice services and paying for hospice related services under other provisions of the plan, in conjunction with relying on case managers to coordinate unbundled services. These plans impose lower lifetime hospice limits, in the range of $5000-$6000. However, when the services have been unbundled, the Unbundled Model purportedly provides a relatively generous benefit. For example, rather than being included within the hospice benefit, medications are covered under the pharmaceutical benefit, medical equipment and supplies by the DME benefit, some counseling by the mental health benefit, and any in- patient respite or hospital care under the inpatient hospitalization benefit. Items not normally covered by the plan, but considered uniquely hospice services, such as pastoral or bereavement counseling or a home health or custodial aide, are covered by the hospice benefit.

| Employer Plan CAn Example of the Unbundled Approach |

| Employer C noted three concerns motivating their adoption of the unbundled approach to structuring their hospice benefit. First, they felt that hospice agencies were inexperienced in dealing with a working population, (i.e., inadequate in providing hospice services for younger people or for those whose primary caregiver was working). Second, they reported that in their experience, hospice providers enrolled patients before they were in need of intense services, and when providers charge the plan on a per-diem basis, the plan is paying an intense-need rate for patients prematurely. The result is that patients reach the plan hospice dollar limit before expiring. In response, Employer C chose to unbundle hospice related services so that they would be paying only for services that the patient was receiving and commensurate with the patient's needs. All but the uniquely hospice services not covered elsewhere in the plan are reimbursed under the hospice benefit. All other hospice-related services, e.g., home health and counseling, are provided under other benefits of the plan. In this manner the employer feels they can "stretch" the hospice dollar and thus actually provide more coverage for custodial care and homemaker services. Employer C also reported that the typical amount of services offered by hospice agencies is insufficient to address the needs of a working population. For example, if a child or spouse of an employee is enrolled in hospice, that employee still needs to attend work in order to maintain health coverage and therefore might need at least forty hours of custodial care per week in order to remain employed. Hospice agencies generally provided only 20 hours a week of custodial or home health care. But Employer C, because of how it has structured its hospice benefit, can provide more than 20 hours of such care per week, if necessary. Another advantage of the unbundling approach, as pointed out by Employer C, is that they are able to arrange for care from more than one hospice provider if it is necessary for insuring continuity of care. The plan's case management is there to arrange for this when necessary. |

Three of the plans we investigated (Employer Plan A, Employer Plan C and Employer Plan I), notably two of the three managed care plans in the study, subscribe to the unbundled model. Each of these places the major responsibility for the coordination of care and payment of services on the case manager employed by the plan. The case manager is responsible for informing the patient about the hospice benefit, enrolling the patient into hospice, determining what services each patient needs, and assessing and implementing the most cost-effective strategy for maximizing the patient's and family's care and comfort. These employers all reported that case management serves an essential function for both the patient and for the plan -- they can be very flexible with what services are offered and how they are billed, and yet they also consider the employer's interests in cost containment. None of these employers felt that the benefit as currently constructed is minimal, and each reported a generally high level satisfaction with the benefit among employees.

| TABLE II-1. Hospice Benefit Offered by Plan Type(N=52) | |||

| Indemnity (N=32) | POS(N=10) | PPO(N=10) | |

| Hospice Benefit Offered(N=46) | 84.4% | 90.0% | 100.0% |

| Hospice Benefit Not Offered (N=6) | 15.6% | 10.0% | 00.0% |

| Total(N=52) | 100.0% | 100.0% | 100.0% |

| TABLE II-2. Characteristics of Hospice Benefit Package by Plan Type(N=46) | ||||

| Characteristic | Indemnity (N=27) | POS(N=9) | PPO (N=10) | Total (N=46) |

| Definition of Hospice Provided | 92.6% | 88.9% | 70.0% | 87.0% |

| Definition of Terminal Illness Specified | 55.6% | 66.7% | 20.0% | 50.0% |

| Other Benefits Reduced if Hospice Elected | 7.4% | 0.0% | 0.0% | 4.3% |

| Precertification Required | 92.6% | 88.9% | 80.0% | 89.1% |

| Deductible for Hospice Benefits | 48.1% | 22.2% | 20.0% | 37.0% |

| Coinsurance for Hospice Benefits (in network) | 40.7% | 44.4% | 30.0% | 39.1% |

| Coinsurance for Hospice Benefits (out of network) | 7.4% | 100.0% | 50.0% | 34.8% |

| Lifetime Limit -- Days | 11.1% | 22.1% | 0.0% | 10.9% |

| Lifetime Limit -- Dollars | 44.4% | 22.2% | 30.0% | 37.0% |

| TABLE II-3. Services Covered Under the Hospice Benefit by Plan Type | |||

| Service | Indemnity (N=27) | POS (N=9) | PPO (N=10) |

| Hospice in Hospital | 81.5% | 77.8% | 40.0% |

| In-Patient Hospice Facility | 77.8% | 88.9% | 20.0% |

| Hospice in an Extended Care Facility/SNF | 48.1% | 33.3% | 20.0% |

| In-Home Hospice | 77.8% | 66.7% | 70.0% |

| Case Management | 44.4% | 66.7% | 50.0% |

| Respite | 40.7% | 11.1% | 20.0% |

| Homemaker | 55.6% | 44.4% | 10.0% |

| Home Health Aide | 42.3% | 44.4% | 50.0% |

| Individual Counseling | 70.4% | 88.9% | 30.0% |

| Family Counseling | 77.8% | 66.7% | 40.0% |

| Equipment | 66.7% | 44.4% | 10.0% |

| Other Therapies | 88.9% | 55.6% | 30.0% |

| TABLE II-4. Characteristics of Plans Selected for Study(N=9) | ||||

| Plans | Plan Type | Number of Covered Lives | Number of Persons Accessing HospiceBenefit 1995 | Hospice Model |

| Employer Plan A | POS | 19,533 | 104 | Unbundled |

| Employer Plan B | PPO | 36,805 | 100 | Comprehensive |

| Employer Plan C | Indemnity | 213,922 | 38 | Unbundled |

| Employer Plan D | Indemnity | 114,825 | 57 | Comprehensive |

| Employer Plan E | Indemnity | 36,871 | 57 | Comprehensive |

| Employer Plan F | Indemnity | 40,508 | 55 | Medicare |

| Employer Plan G | Indemnity | 184,115 | 45 | Medicare |

| Employer Plan H | Indemnity | 6,965 | 19 | Comprehensive |

| Employer Plan I | POS | 45,167 | 0 | Unbundled |

III. HOSPICE-RELATED UTILIZATION AND EXPENDITURES OF THE PRIVATELY INSURED

A. Overview

This section summarizes utilization and expenditure analyses related to hospice use among privately insured persons. We begin with a description of MEDSTAT's MarketScan® Database upon which the analyses are based. Many of the utilization and expenditure analyses were conducted on episodes of hospice care. Thus, we also describe our episode construction methodology, and its limitations.

B. The MarketScan® Database

Analyses in this section rely on 1994 through 1996 data from The MEDSTAT Group's MarketScan Database. The analytic focus of this study is on hospice use by the privately insured in 1995. However, since we are interested in examining episodes of care, claims/utilization data from 1994 and 1996 augment the 1995 data, as episodes occurring in 1995 may have started in 1994, or may have extended into 1996. For this analysis, we selected fee-for-service plans (Indemnity, Preferred Provider Organizations, and Point of Service Plans) for active employees, early retirees and their dependents. Plans with sufficient data quality to support this analysis were retained, representing slightly over four million insured covered lives in 1995. Tables III-1 through III-4 provide basic demographic information on these four million covered lives in 1995. The term "covered lives" refers to all individuals (i.e., employees, spouses and dependents) who are eligible for health care coverage provided by any of the employers included in the analytic database. "Covered lives" represents all eligible enrollees who could have potentially used inpatient or outpatient services, regardless of whether such enrollees actually consumed these services within the study's time frame.

Just about two-thirds of the covered lives in the MarketScan Database are comprised of the employee (42.7 percent) or spouse (24.4 percent), with the remaining covered lives consisting of dependents. Employee status, i.e., active or retired, is assigned to all family members based upon the employee's work status. About three-quarters of the covered lives have an employee status of "Active" (either full or part time). Less than 10 percent of the covered lives have an Employee Status of "Retired", consisting solely of early retirees (not Medicare eligible) or their dependents. Under one percent of the covered lives are no longer actively working for the employers and are COBRA continuees or on Long Term Disability. (Data not shown; see Appendix B, Table B-1 and Table B-2.)

Not surprisingly, since the MarketScan data is employer-sponsored, the age of individual beneficiaries is predominantly under age 65, in large part reflective of the working-age population and their dependents. As shown in Table III-1, the 0 to 17 age group accounted for the largest percentage of covered lives (25.5 percent). About 48 percent of all covered lives were male and 52 percent were female.

The Southern region of the country contributed the highest concentration of covered lives, with about 38 percent of the total, followed by the North Central region (27 percent), the "unknown" region (13 percent), the West (13 percent) and the Northeast (9 percent). (See Table B-3 in Appendix B for details.)

C. Definition of Hospice Service Utilization

In the MarketScan database, hospice services can be identified in one of two ways: (1) as a hospice type of service; or (2) as a service delivered by a hospice provider. For the purposes of this study, hospice service use was operationalized as a claim record designated by either a hospice type of service or a hospice type of provider. Using this definition, 1,910 persons were initially identified as hospice users.

Upon examination of diagnosis codes, however, it appeared that a small subset of these individuals did not have a diagnosis consistent with a terminal illness and did not have use patterns suggestive of terminal illness. Those we eventually considered unlikely to have a terminal illness also did not have health care expenditures in the 60 days prior to the date of service on the hospice claim. The absence of any health care utilization in the 60 days preceding hospice initiation would be an unusual occurrence if a person were indeed terminally ill. All of the beneficiaries in question also had insurance coverage through the same insurance carrier/claims administrator, a fact which pointed to possible miscoding of hospice services by this particular carrier. This group consisted on 196 beneficiaries. A physician, David Schutt, M.D., Associate Medical Director at The MEDSTAT Group, reviewed the suspect diagnosis codes on hospice claims for this subgroup of patients. Following review by Dr. Schutt, 175 of the suspect hospice recipients were deemed coded erroneously. Of the 196 suspected of not receiving hospice, 21 were retained and treated as hospice recipients in subsequent analyses. Once this adjustment was made 1,735 persons were defined as users of hospice services in 1995.

D. Characteristics of Hospice Users in the MarketScan Database

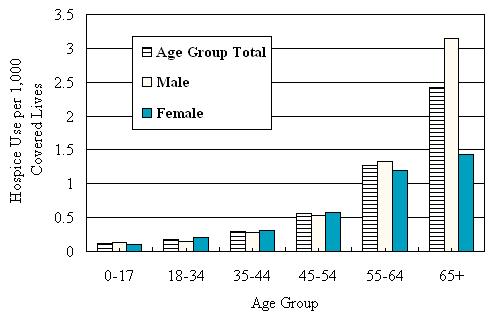

The age distribution of hospice users differs markedly from the age distribution of all enrollees in the database. As shown in Table III-2, the largest group of hospice users is in the 55 to 64 year old age category, representing 42 percent of the hospice users, whereas the younger age groups predominate in the insured population as a whole. Indeed, those in middle- to late-middle-age (35-54 years) account for slightly over one-third of hospice users in this commercially insured population. The average age for hospice users was 48.9 years. Users are almost evenly split between males and females.

Figure III-1 graphically displays the rate of hospice use by age and sex and shows an increased risk of hospice use with age. Hospice use rates for males and females in each age group were very similar, except in the over 65 age group, where the rate for males was approximately double the rate for females. Nevertheless, use is clearly associated with age. Starting with the 35-44 age group, the risk of use nearly doubles for each succeeding age group. However, the use of hospice care, even for the oldest age categories, is very low. For example, in the age 65+ category only 2.4 persons in 1,000 use hospice services. Indeed, for all age groups combined the hospice use rate per 1,000 covered lives was only 0.43, i.e., less than one person in 1,000. Compared to other service types, the magnitude of hospice use is extremely low in this population.

The largest proportion of hospice users resided in the Southern region (38 percent), followed by the North Central region (27 percent). The Northeast and West regions contributed the smallest proportion of users (13 percent each). This distribution closely parallels the regional distribution of covered lives in the MarketScan Database as a whole. (See Table B-3 and Table B-4 in Appendix B for more detail.) Use rates were highest in the Northeast (0.60 hospice users per 1,000 covered lives), followed by the North Central region (0.46 per 1,000), the South region (0.44 per 1,000), the West region (0.43 per 1,000) and the "unknown" region (0.23 per 1,000) (See Table B-5 in Appendix B.)

Over half of the individuals using hospice services were employees (58.6%), nearly one-third were spouses (32.7%) and 8.7% were classified as dependents. (See Table B-6 in Appendix B for details.) Rates of hospice use are a function both of employee status and the relationship of the hospice user to the policy holder. As Table III-3 shows, rates of use are highest when the user is on long term disability, is invoking COBRA, or has opted for retirement -- all statuses consistent with a non-active work status due to terminal illness.

E. Hospice Episode Construction Methodology

Hospice episodes of care were developed in order to group all of an individual's entire hospice and non- hospice claims experience (all service types and costs) associated with a period of hospice utilization. Below we describe our episode construction methodology, including patient selection, episode initiation, and episode termination.

First, beneficiaries with at least one health care claim in 1995 with hospice service use indicated by hospice type of service or hospice provider type were selected. All healthcare claims (hospice and non-hospice) in the 1994 through 1996 time period for these individuals were then compiled. Episode initiation was defined as the date of the first hospice claim for which there was a preceding 60-day "clean period" where no hospice utilization occurred. Episode termination was determined by identifying the date of a hospice claim that was followed by a 60-day "clean period". It was also possible for an episode to be terminated by a beneficiary's disenrollment from the insurance plan (due to death or otherwise), in which case there would not be a 60-day post-episode clean period.5

The focus of the study is on hospice use during the 1995 calendar year. However, since episodes presumably span more than one calendar year, we also used the 1994 and 1996 MarketScan data in order to construct 1995 hospice episodes that began in 1994 or ended in 1996. That is, if a hospice episode and accompanying 60-day clean periods both pre- and post-hospice utilization were completely contained in 1995, then 1994 and 1996 utilization data were not necessary. However, if a person was in the midst of a hospice episode on January 1, 1995, then the 1994 experience for that person was searched for the beginning date of the hospice episode in 1994 until a 60-day clean period prior to the episode was established. Similarly, when necessary, hospice episodes were continued into 1996 in order to determine a valid episode termination date.6

In the analyses that follow, utilization prior to the hospice episode (pre-episode) and, where appropriate, following the hospice episode (post-episode), is presented, along with utilization during the episode. However, because a small segment of our sample (4.3 percent) experienced more than one hospice episode, it is possible that a given claim(s) may be counted as both in the "pre-episode" period and the "post- episode" period. The example in Figure III-2 below illustrates this scenario.

In this example, the beneficiary was selected as part of the sample since hospice utilization occurred in 1995. The 2/2/95 claim is the earliest hospice claim in 1995. Since a 60-day clean period (without hospice use) must be established at the beginning of each episode, the 1994 claims were searched for hospice experience. This query resulted in one earlier hospice service on 12/11/94, which is considered as the beginning of the first episode. The 2/2/95 claim ends the first episode because more than 60 days elapsed before the next hospice claim occurred. The 5/9/95 hospice claim starts the second episode. This episode is extended to 5/31/95 since the next hospice service occurs within 60 days. It is extended again to include the 7/15/95 hospice claim, which occurs within 60 days of the prior hospice claim. No other hospice claims occurred within 60 days following the 7/15/95 claim, and thus the 7/15/95 date becomes the episode end date. The 3/29/95 non-hospice claim does not fall within a hospice episode, but since it falls within 60 days of both the first hospice episode and the second hospice episode, it is in both the "post-episode" period of the first episode and the "pre-episode" period of the second episode.

F. Hospice Episodes Among the Commercially Insured

In this section we describe the nature of hospice episodes among persons commercially insured and using hospice services. These analyses were conducted at the episode level (or claim-level), not at the enrollee/patient level (as in Section III-D above). Episode length was typically extremely short as indicated by the median value of 1.0 shown in Table III-4. Note, however, that the mean was 21.4 days, with a relatively large standard deviation (51.6). Only 41 percent of episodes exceeded 1 day in duration (data not shown). Nearly all beneficiaries using hospice services had only one hospice episode. Fewer than 5 percent of the patients experienced more than one episode, as can be seen in Table III-5.

In an attempt to explain the preponderance of one-day episodes, we contacted three employers whom we had originally interviewed and whose plans had moderate-to-high rates of 1-day episodes. None of them were able to provide us with any insights as to the possible reasons behind this phenomenon. We speculated with them that it may be due to one of four factors. First, it may be an artifact of claims processing, i.e., bundled billing (one claim representing more than one service date). Second, the literature points to the reluctance of physicians to refer to hospice in general. And that when most physicians do refer death is often immanent. Patients and families, too, are reluctant to accept hospice, as it is tacit acknowledgment that "there is no hope". And thirdly, it may be possible that some of the one-day stays are for assessment for hospice that is subsequently rejected by the patient and/or family. Unfortunately, none of our employer informants was able to shed light on this issue. It remains a question for further research. Finally, there is the possibility that some of the claims were coded as hospice claims erroneously; however we suspect that this is a remote possibility since the diagnoses and procedures on the claims were consistent with the need for hospice.

The top 20 ICD-9-CM diagnosis codes associated with hospice episodes are largely dominated by terminal/chronic illnesses such as cancer, AIDS, COPD, Heart Disease and Amyotrophic Sclerosis (ALS) (Table III-6). The top 20 diagnosis codes account for 43 percent of all diagnoses related to hospice use. Note that the unit of analysis in Table III-6 is the claim, rather than the episode. The complexity of aggregating the diagnoses to the episode or person level would be time-consuming, and was considered beyond the scope of this project.

Table III-7 presents data comparing the prevalence of given diagnoses among the commercially insured (MarketScan database) with the prevalence of diagnoses of a sample of hospice patients nationally (based on the 1996 National Home and Hospice Care Survey -- NHHCS). Although hospice users in the MarketScan database are substantially younger (primarily under 65 years old) than hospice users in the 1996 NHHCS (about two-thirds 65 years and older), the distribution of hospice diagnosis codes is relatively similar for the two. About half of the all-listed diagnoses in both the NHHCS and MarketScan were malignant neoplasms. The NHHCS population had a higher percentage of circulatory disorders and heart disease (17.2 percent and 8.6 percent respectively) than MarketScan (5.7 percent and 4.1 percent). The MarketScan population had a higher percentage of infectious disease diagnoses (5.1 percent versus 2.7 percent), a category that includes AIDS.

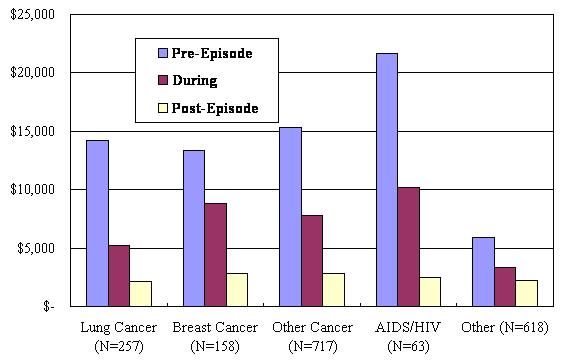

The data presented thus far do not isolate the major condition responsible for the terminal status, and thus, presumably, for the hospice use. Unlike Medicare hospice claims which record such information, the MarketScan database merely records diagnoses associated with each claim; no diagnosis is given primary status nor is there a diagnosis identified as the reason for the hospice use. Thus, we devised a hierarchical strategy for assigning a "terminal" diagnosis to each hospice episode. First, episode diagnoses were scanned for AIDS, AIDS-related and HIV diagnoses. Episodes with these diagnoses were placed in the AIDS/HIV category; given the hierarchical nature of our methodology, even if other "terminal" diagnoses such as cancer were identified as associated with the episode, the terminal diagnosis episode was classified as AIDS/HIV. All episodes are classified in only one category. If an episode was not associated with an AIDS/HIV diagnosis, then the list of diagnoses was scanned for lung cancer, followed in order by breast cancer, and then cancers in other site. Just about two-thirds (65.9 percent) of episodes were classified into one of these categories. The "terminal" diagnosis for the remaining episodes was classified as "Other" since no one diagnosis predominated among the remaining third of the episodes.

Using this methodology for identifying the terminal condition, Table III-8 reports on the prevalence of the terminal conditions, at the episode level, by sex. This table reveals that the most prevalent diagnosis for hospice episodes was cancer other than cancers of the breast and lung (39.5 percent of episodes). This holds true for episodes experienced by both males and females. Second in prevalence were "Other" terminal diagnoses (34.1 percent). Not surprisingly, lung cancer diagnoses were more prevalent for episodes experienced by men (17.6 percent) than for women (10.9 percent), and breast cancer was more prevalent for episodes experienced by women (16.7 percent) than by men (0.3 percent). We suspect that the relatively high rate of AIDS/HIV episodes (3.5 percent) reflects the predominance of the working-age population within the MarketScan database. Little difference in episodes was experienced by the beneficiary holder (typically the employee) versus episodes experienced by spouses of the employee (See Table B-6 in Appendix B), where approximately two-thirds of the episodes are cancer-related. Episodes experienced by dependents, a much younger group of hospice users in general, showed a very different pattern; 86.5 percent of their episodes were assigned to the "Other" category, reflecting congenital disorders and other terminal diseases associated with childhood.

Regional differences also emerged (Table III-9). Non-cancer/non-HIV/AIDS episodes were just about twice as prevalent in the Northeast and North Central regions (48.9 percent and 43.2 percent, respectively) than they were in South and West (24.5 percent and 24.7 percent, respectively). The prevalence of AIDS/HIV episodes was slightly higher in the South and West, and cancer episodes in these regions were substantially higher (approximately 70 percent of episodes in the South and West, but only 49 percent and 54.9 percent in the Northeast and North Central regions, respectively). These results do not reflect the distribution of regional cancer death rates or AIDS-related deaths, where the Northeast and North Central sections of the country report the highest cancer related deaths. AIDS-related deaths are highest in the Northeast, followed by the South, West, and North Central regions. We suspect, rather, that the regional differences in cancer and AIDS diagnoses among the MarketScan population of hospice users may reflect physician referral patterns and hospice penetration rates in the different regions of the country.

When the age of beneficiaries experiencing the episodes are examined by condition (Table III-10), we observe the average age of cancer patients with hospice episodes ranged from the mid to late 50s. Younger average ages, hovering around 40, are associated with AIDS/HIV and "Other" diagnoses. The predominance of the middle years reflects, once again, the dominance of the working-age population in the MarketScan database.

Despite an overall median of 1 day for episode duration (as noted above), duration seems to vary somewhat by terminal condition (Table III-11). The median episode duration for AIDS/HIV was the highest at 11 days, followed by breast cancer episodes (6 days), and lung cancer episodes (4 days). For all other conditions median episode duration was 1 day.

G. Health Care Utilization for Commercially Insured Hospice Patients

This next section reports on service utilization associated with hospice episodes in three distinct periods:

- 60 days prior to the beginning of the hospice episode (pre-episode);

- during the hospice episode; and

- 60 days following the end of the hospice episode (post-episode).

At first glance it may seem incongruous to be examining the period following the end of the hospice episode (post-episode period), since one would expect that the termination of a hospice episode would to be due to death and thus "post hospice utilization and expenditure experience" an oxymoron. However, it is quite conceivable for utilization to occur in a post-episode period in this population. The commercially insured are not typically locked-into a hospice benefit once they have chosen it. Under the majority of policies, as our discussions with commercial plans demonstrated, an enrollee may opt out of hospice care at any point (or may even be receiving both curative and palliative care at the same time).7

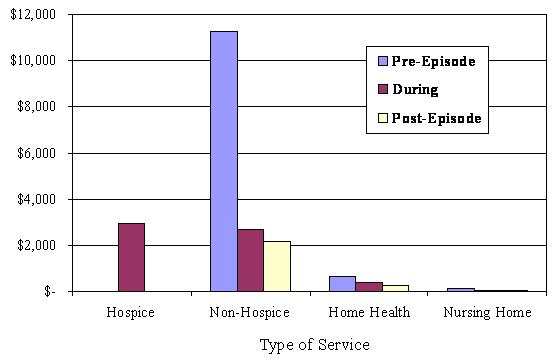

In the following analyses, hospice services are divided into inpatient and outpatient categories, representing the place of service -- either a confinement in any inpatient setting or services received in an ambulatory/outpatient setting (including the patient's home). Because there is interest in understanding whether hospice care is supplemented by non-hospice home health and/or nursing home care among commercially insured hospice users, our analyses also include home health and nursing home utilization. All utilization not classified as hospice, home health or nursing facility care is categorized as non-hospice services. Non-hospice services are further classified as delivered in an inpatient or outpatient setting. Payments are defined as the total reimbursement made for the service to the provider of care from all sources of payment (i.e., plan, enrollee out-of-pocket and coordination of benefits amounts).

Not surprisingly, almost all of the hospice episodes (92.7 percent) were preceded with service use in the 60 days prior to the episode (Table III-12). Interestingly, over half of episodes (59.3 percent) were followed by service use. Combined with our earlier finding that the median length of hospice episodes is 1 day, this suggests that a substantial proportion of commercially insured hospice users use hospice only fleetingly, and tend not to embrace hospice as a major source of care in the course of their terminal illness.

Table III-12 also shows that hospice services for the commercially insured are mainly delivered in the outpatient setting, i.e., 88.6 percent of hospice episodes were associated with hospice care delivered in an outpatient setting. A much smaller percentage (16.3 percent) of the episodes was associated with inpatient hospice services (either a hospice facility or another inpatient facility). In 4.9 percent of episodes, patients received hospice care in both settings.

Nursing home services were utilized very rarely during a hospice episode, i.e., in less than one percent of episodes -- and only slightly more frequently before and after the episode, 2.1 percent and 1.0 percent, respectively. This pattern is consistent with restrictions on nursing home use in commercial plans where nursing home care is usually limited to the time period after an inpatient admission, typically with a 30-day restriction. Conversely, home health services were utilized more frequently both before, during, and after the hospice episode. Home health use was most prevalent in the pre-episode period (31.1 percent of episodes), and less prevalent during the hospice episode (15.7 percent) and following the episode (16.7 percent). There is some evidence, therefore, for the contention that home health services are used in conjunction with, and as supplement to, hospice care.

It is also interesting to note that in 54.9 percent of the episodes non-hospice services were utilized during the hospice episode concurrently with hospice services. Thus, it is clear that during the hospice episode commercially insured hospice patients continue to receive other medical treatments in addition to hospice services. It is unknown to what extent curative treatments were provided for the terminal illness and/or non-hospice services were provided for conditions unrelated to the terminal illness (versus for the management of symptoms related to the terminal condition). By law, hospice services provided under Medicare are restricted to palliative care, and the provision of non-hospice services are restricted to the care of conditions unrelated to the terminal illness. However, among the commercially insured, as we know from our discussions with employers and plans (see Section II of this report), many plans do not require forfeiture of curative treatment when the hospice benefit is invoked.