KEY POINTS:

- Due to temporary legislative changes and regulatory approaches that weakened program integrity safeguards, the ACA Exchanges experienced unprecedented enrollment growth from 2021 to 2024, nearly half of which was suspected to be improper, phantom, or fraudulent.

- Enrollment that is improper or fraudulent is enrollment by individuals misstating their income to gain access to free plans. Phantom enrollees are unknowingly enrolled in free plans by brokers or auto enrolled. By our estimate, improper, phantom and fraudulent enrollment peaked at 5.6 million people in 2025.

- In 2025, the Trump Administration issued the Marketplace Integrity and Affordability Rule, which took significant measures to ensure those receiving subsidies were actually eligible for those subsidies.

- Currently, an estimated 19.2 million Americans are enrolled in ACA Exchange plans. This figure is higher than every year prior to 2024.

- The Trump Administration has utilized numerous tools mobilizing a full-scale effort to ensure federal subsidies are going only to those for whom they are intended. Trump Administration program integrity efforts stopped about 1.5 million enrollees from receiving subsidies they did not qualify for and ended or blocked another 1.4 million through February 2026, for a total of 2.9 million people who had previously been improperly receiving subsidies they did not qualify for.

- Unfortunately, improper, phantom, or fraudulent enrollment persists. Recent experience during and after the 2026 Open Enrollment Period strongly suggests ongoing and persistent fraud, waste, and abuse in the system. We estimate 2.6 million improper and phantom enrollments remain, including over 1 million enrollments without a social security number.

- The Trump Administration remains committed to aggressively rooting out waste, fraud, abuse, and corruption to protect Americans from unscrupulous brokers using their information to secure payments from the federal government and safeguard the program’s long-term stability for those that depend on it.

BACKGROUND

Prior to the COVID-19 pandemic, about 10 million people enrolled in Affordable Care Act (ACA) Exchange plans annually, on average. In 2021, the American Rescue Plan Act (ARP) created a temporary enhancement of subsidies that increased the share of premium covered by the federal government, with enrollees with incomes between 100 and 150 percent of the federal level (FPL) expected to pay 0 percent of family income towards benchmark plan coverage. These subsidies were later extended through 2025 through the Inflation Reduction Act (IRA).1

This law, coupled with actions from the Biden-Harris Administration, created the incentive and opportunity for fraudulent, phantom, and improper enrollments. Phantom enrollees are unknowingly enrolled in free plans by brokers or auto enrolled and improper enrollment is enrollment by individuals misstating their income to gain access to free plans. By making zero premium plans available to individuals with incomes between 100 and 150 percent of the federal poverty level (FPL) and removing basic eligibility checks, agents and brokers were able to earn commissions, at scale, by improperly or fraudulently enrolling people, often without their knowledge, given they owed no premium.2 In addition, enhanced direct enrollment (EDE), available only on federally facilitated exchanges (FFEs) and state-based exchanges using the federal platform (SBE-FPs), let brokers enroll consumers without identity proofing.3,4 Brokers earn $5-$30 per-member-per-month and facilitated 78 percent of active plan selections by 2024, up from 55 percent in 2021- a considerable financial incentive.5,6 In 2025, CMS canceled coverage for 250,000 people enrolled without consent and identified 200,000 unauthorized plan switches.7 HHS is not the only federal government agency to cite program integrity concerns with the ACA Exchanges. The Government Accountability Office (GAO) has repeatedly concluded that historically CMS had not fully implemented a comprehensive fraud risk management framework for the federal exchange and that major vulnerabilities have existed.8,9,10,11,12,13

This Issue Brief describes (1) the state of ACA Exchange enrollment, (2) suspected improper, phantom, and fraudulent enrollment resulting from recent federal policies intended to be temporary responses to the pandemic, and (3) steps the Trump Administration is taking to root out waste, fraud, and abuse to preserve federal programs for those who need them most.

DATA AND METHODS

This Issue Brief uses data from the 2019-2024 Enrollee-Level External Data Gathering Environment (EDGE) ACA Exchange claims data. We provide descriptive statistics on total zero premium enrollment by income group as well as zero claiming by income group, to highlight the connection between zero premiums and zero claiming. Finally, we highlight spikes in zero claiming among enrollees eligible for free net of subsidy coverage, which is highly suggestive of improper or fraudulent enrollment by brokers. Namely, individuals enrolled without their knowledge—made significantly easier when no premiums are due to alert the individual—will not have medical claims.

FINDINGS

Zero Premium Plans Were Never Part of the ACA Exchange Design and Create Incentives for Fraud

During the debate over the enactment of the ACA in 2009 and 2010, lawmakers did not consider providing free plans in the private insurance marketplace. Instead, the law set up a minimum contribution amount—2 percent of income—for a benchmark plan. There is good reason for this minimum contribution. When insurance companies are forced to compete for enrollees who must contribute their own money to a plan—even a modest amount—they are forced to offer plans that an enrollee will find commensurately valuable14.

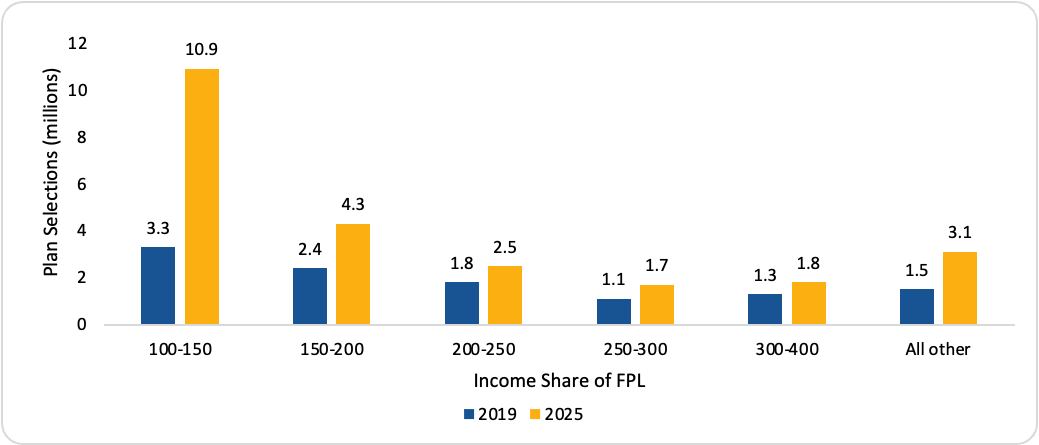

Making benchmark premiums for people with incomes between 100 and 150 percent of FPL free, contributed to an environment where dishonest commission seeking brokers, had incentive and opportunity to sign up unknowing people, providing no benefit to such individuals who cannot use coverage they are not aware of.6 The vast majority of new enrollments since the enhanced subsidies were enacted has been among enrollees eligible for zero premium plans net of subsidy (Figure 1). From 2021-2025, total enrollment increased by 12.9 million. By comparison, enrollment among individuals with incomes between 100 and 150 percent of FPL (eligible for zero premium plans) increased by 7.6 million—59 percent of the total increase.

Figure 1: ACA Exchange Selections during the Open Enrollment Period by Federal Poverty Level, 2019 vs 2025

Note: The data in this table represent total individuals who have selected an ACA Exchange plan (with or without the first premium payment having been received directly by the ACA exchange or the issuer) during the 2019 and 2025 Open Enrollment Periods by Federal Poverty Level (FPL). The income reported is the household income attested by the applicant or is based on verified data from a prior year. FPL is calculated for the contiguous states and separately for Alaska and Hawaii as per federal guidelines from the household income reported. From: https://www.cms.gov/data-research/statistics-trends-and-reports/marketp….

Removing Eligibility Verifications Enabled Potential Abuse of $0 premium Plans

The opportunity for fraud created by temporary access to $0 premium net of subsidy benchmark plans was exacerbated by federal policies that allowed year-round enrollment for such plans and removed prior eligibility verifications15. As enacted, the ACA included several provisions aimed at protecting the new Exchanges from improper or fraudulent enrollment. The law includes a clear framework for verifying whether people are eligible for premium subsidies.16 In addition, the ACA Exchanges had limited enrollment periods, similar to those for enrollees in group coverage, to avoid adverse selection of individuals only enrolling when sick and needing care. These statutory verification standards and enrollment periods were rolled back by federal regulations during the COVID-19 pandemic under the Biden-Harris Administration. Below, we list the top ten federal policies that weakened program integrity.

- Creating an SEP to enroll people year-round with incomes between 100 and 150 percent of FPL.

- Removing pre-enrollment verifications for all but the loss of minimum essential coverage SEP.

- Rescinding income verifications for people who report income above 100 percent of FPL when data sources show income below 100 percent FPL.

- Allowing applicants to attest to income when the IRS did not have tax information to verify their income.

- Extending the time to verify income from the statutory 90 days to 150 days, allowing premium subsidies and commissions to be continually paid.

- Requiring Exchanges to wait to end subsidies for an extra year after an enrollee failed to file taxes and reconciled their APTC.

- Requiring carriers to enroll people who previously failed to pay their premium.

- Stopping periodic checks to ensure people were not dually enrolled in Medicaid.

- Stopping checks on whether people had failed to file their taxes and reconcile their APTC.

- Extending the Open Enrollment Period

High Levels of Suspected Improper and Fraudulent Enrollments

In 2024, several third parties and media outlets began reporting a significant increase in suspected improper, phantom, or fraudulent enrollment in ACA Exchange plans coinciding with federal regulatory changes and the availability of $0 premium plans as a result of the enhanced subsidies.18,18,19,20

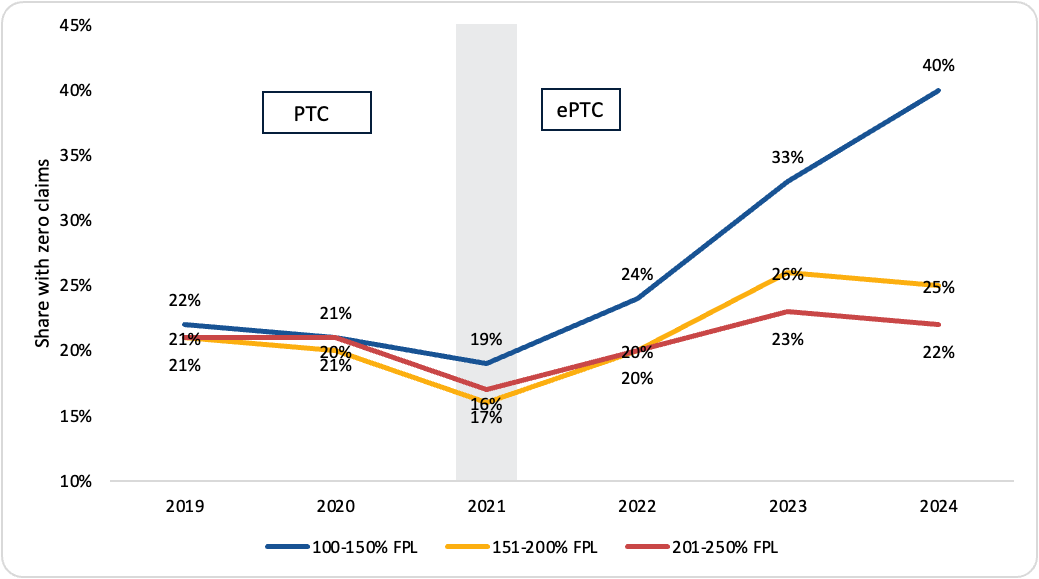

Figure 2 highlights the potential fraud by showing a spike in zero claiming among low-income enrollees after 2020. We cannot observe income in the claims data, so we proxy for income share of the federal poverty level (FPL) with the silver CSR plan variety selection the individual is enrolled in. During the 2024 open enrollment period, 77.2 percent of enrollees with incomes between 100 percent of the federal poverty level (FPL) and 150 percent of FPL chose silver plans (and are automatically enrolled in a silver 94 plan conditional on a silver plan selection). Most in the 150 to 250 percent income range, 62.8 percent, chose silver plans.21 Enrollees with the lowest income experience the largest increase in zero claiming. This group is also the group that is newly eligible for free net of subsidy coverage. It is well known that poorer individuals are less likely to use healthcare (more likely to have zero claims), but this does not explain a jump in this group’s likelihood of using no healthcare after coverage becomes free after 202022. A record high 40 percent of individuals enrolled in $0 premium cost sharing reduction plans (100-150 percent of FPL) had zero claims in 2024. By contrast, for plans where even a modest premium is charged, the percentage of plans with zero claims has largely remained under 25 percent. This may signal an uptick in fraudulent or improper enrollment by agents and brokers leveraging the fact that the poorest enrollees are not required to pay a premium, and therefore receive no bill and can be enrolled without their knowledgea. The trends, especially for the 100 to 150 percent FPL group, run counter to what we observed about care seeking patterns in 2020-2021. People were less likely to seek care during this period and then care use accelerated in 2022-2024, the opposite of what we see in Figure 223.

Figure 2: Zero Claims Rates Concentrated Among Those Eligible for Zero Premium Plans.

Notes: CCIIO analysis of 2019-2024. We identify enrollments by FPL by using the number of enrollees in each silver/CSR plan and derive the FPL by the CSR variant, since only those with incomes between 100-150 percent of FPL are eligible for the silver 94 plan, only those with incomes between 151-200 percent of FPL are eligible for the silver 87 plans and only those with incomes between 201-250 percent of FPL are eligible for the silver 73 plan. Thus, the data presented is for a subset of exchange enrollees in each income group since not all those that are eligible necessarily select these plans.

Last year, two stark examples demonstrating improper enrollment came to light. CMS discovered 1.6 million ACA exchange enrollees that were simultaneously enrolled in multiple types of insurance paid for entirely by the Federal government in 202424. Beyond fiscal integrity concerns associated with suspected fraudulent or improper enrollees could incur surprise tax liabilities, delayed access to medications, or care denials as a result of policies that limit program integrity measures.25

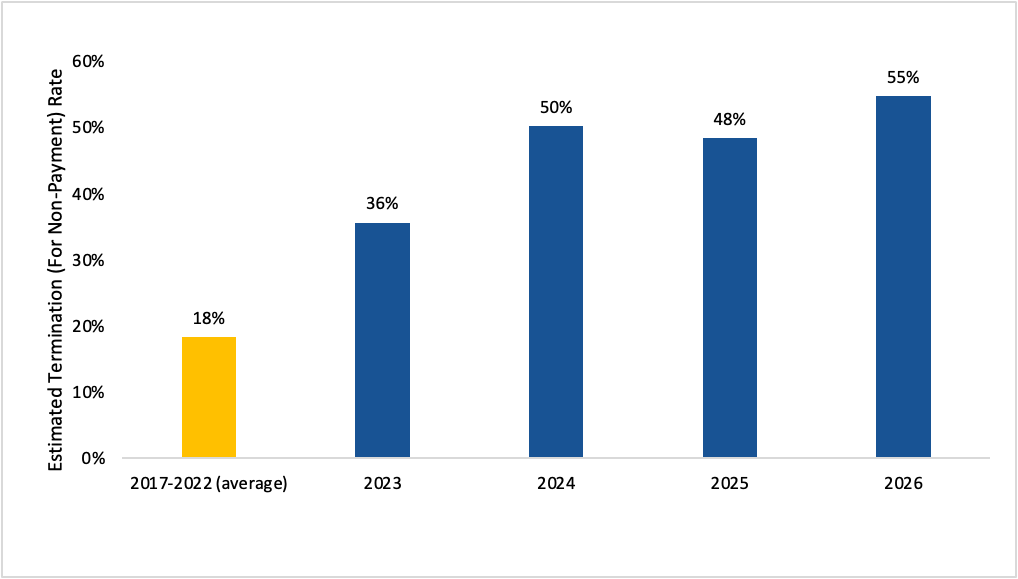

Beginning in 2023, HealthCare.gov [the Federally Facilitated Exchange (FFE)] began experiencing a sharp uptick in the proportion of people who failed to pay their premium after being re-enrolled automatically from a $0 plan to a plan with a premium. Historically, on average, 18 percent of people who newly owe a premium following auto re-enrollment from a $0 premium plan end up having their coverage terminated for non-payment of premiums (Figure 3). Over the past three years (2024-2026), around 50 percent of those newly subject to a premium are estimated to have failed to pay and became termed out of coverage, suggesting a substantial portion were unaware they were enrolled, did not exist, or did not derive sufficient value from their coverage.b

Figure 3: Estimated Premium Non-Payment, 2017-2022 relative to 2023-2026, FFE States.

Note: CCIIO analysis of ACA Exchange effectuated enrollment data. Sample: Individuals who had been enrolled in zero premium plans, but were auto re-enrolled into plans with non-zero premium.

In 2025, the Trump Administration proposed and finalized a set of program integrity and affordability policies designed to stabilize the market, lower premiums, and end vulnerabilities potentially leading to improper and fraudulent enrollment as part of the 2025 CMS Marketplace Integrity and Affordability Final Rule.26 The rule strengthened income verification by requiring additional documentation when IRS tax data are unavailable or inconsistent with an applicant's reported income, eliminated the automatic 60-day extension for resolving income verification issues, and reinstated the policy denying advance premium tax credits (APTCs) to individuals who failed to file and reconcile their taxes after one year rather than two. It also reinstated pre-enrollment verification for Special Enrollment Periods (SEPs) on the federally facilitated exchanges, eliminated the monthly SEP for individuals with incomes below 150 percent of the federal poverty level, and required many automatically re-enrolled consumers with a $0 premium to contribute a temporary $5 monthly premium until they actively confirmed their eligibility. The rules were subsequently stayed by the United States District Court for the District of Maryland, limiting the Trump Administration’s ability to address fraudulent and improper enrollments27.

The rule strengthened income verification by requiring additional documentation when IRS tax data are unavailable or inconsistent with an applicant's reported income, eliminated the automatic 60-day extension for resolving income verification issues, and reinstated the policy denying advance premium tax credits (APTCs) to individuals who failed to file and reconcile their taxes after one year rather than two. It also reinstated pre-enrollment verification for Special Enrollment Periods (SEPs) on the federally facilitated exchanges, eliminated the monthly SEP for individuals with incomes below 150 percent of the federal poverty level, and required many automatically re-enrolled consumers with a $0 premium to contribute a temporary $5 monthly premium until they actively confirmed their eligibility. The rules were subsequently stayed by the United States District Court for the District of Maryland, limiting the Trump Administration’s ability to address fraudulent and improper enrollments27.

Current Enrollment Levels Reflect the Removement of Fraud, Waste and Abuse

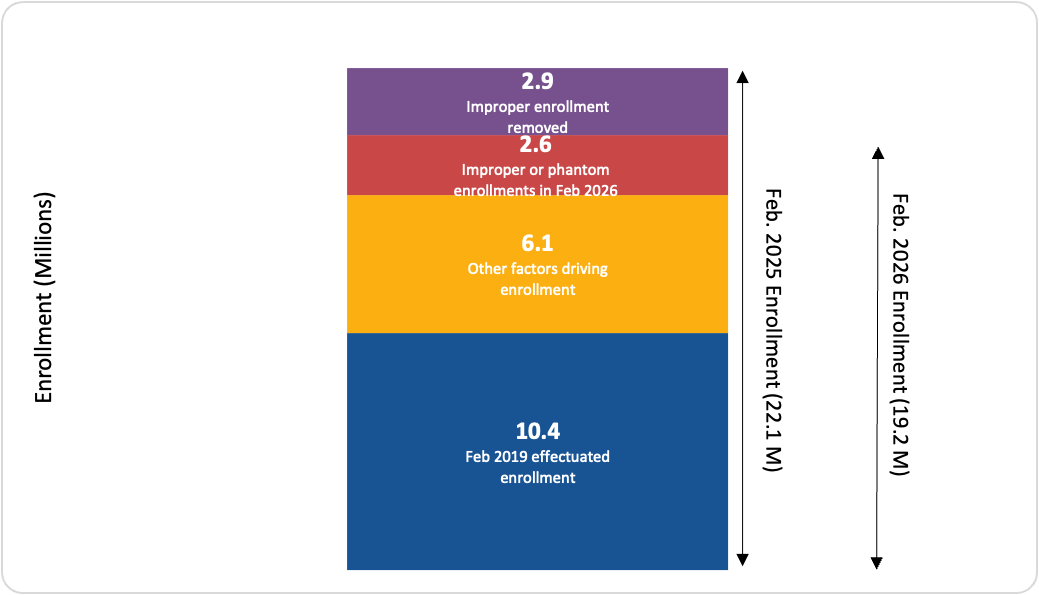

As of February 2026, an estimated 19.2 million individuals are enrolled in ACA Exchange plans. This enrollment level is higher than every year prior to 2024 and nearly double historical enrollment levels (Figure 4). Looking at enrollment figures alone lacks critical context surrounding the suspected levels of improper and fraudulent enrollment that grew under recent federal policies and still persist today following the initial court injunction that prevented CMS from implementing critical program integrity safeguards20. CMS estimated that as many as 4.4 million of 2024 enrollments were fraudulent or improper28. This accounted for nearly half of the new enrollment since the enhanced subsidies were passed in 2021. CMS estimates this number grew to 5.6 million in 2025. These estimates of fraudulent enrollment reflect the difference between observed enrollment, estimated transitions into ACA Exchange coverage from other sources (other factors driving enrollment) and the 2019 baseline.

Figure 4: Improper and Phantom Enrollment in ACA Exchange Plans, 2019-2026.

Note: CCIIO analysis of February Effectuated Enrollment as of 4/15/2026, 2019-2026.

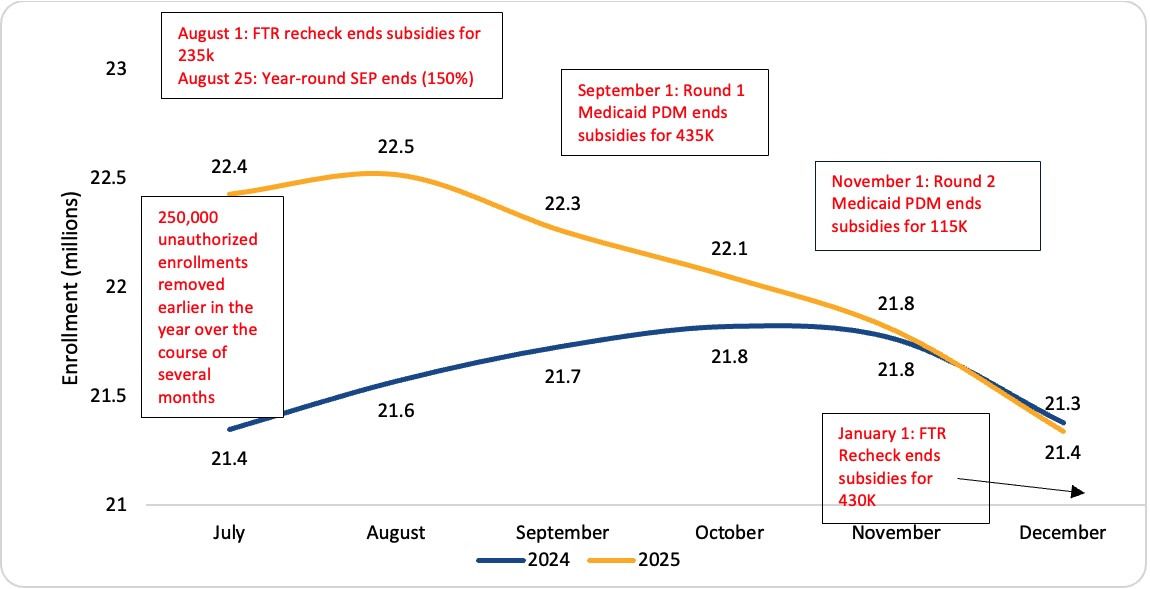

Despite critical provisions of the Marketplace Integrity and Affordability rule being stayed, CMS has been able to remove approximately 1.5 million of the estimated 5.6 million improperly enrolled individuals29. This includes enrollees who had not qualified for coverage because they were dually enrolled in Medicaid/CHIP, had not filed or reconciled their taxes, or never authorized the enrollment to begin with. We estimate another 1.4 million have either been removed or blocked from enrollment due to additional program integrity measures such as ending the year-round enrollment period for people with incomes between 100 and 150 percent of FPL (Figure 5).

Figure 5: Total Effectuated Enrollment by Month, 2024 vs. 2025 (July-December), Compared with Policy Changes.

Notes: Medicaid Periodic Data Matching (PDM) is a CMS program integrity process that compares Medicaid and Children's Health Insurance Program (CHIP) enrollment records with Affordable Care Act (ACA) Exchange enrollment records to identify people who are enrolled in both programs simultaneously. Because most people enrolled in Medicaid or CHIP are not eligible to receive Advance Premium Tax Credits (APTCs) for ACA Exchange coverage, these matches help prevent duplicate federally subsidized coverage. The FTR Recheck or the Failure-to-File-and-Reconcile Recheck is a follow-up verification process used by CMS after the initial Open Enrollment Period to determine whether ACA Exchange enrollees who said they had filed and reconciled their Advance Premium Tax Credits (APTCs) actually did so. Enrollment in the figure is national enrollment, while numbers in text boxes refer to subsidy removals for FFE removals only.

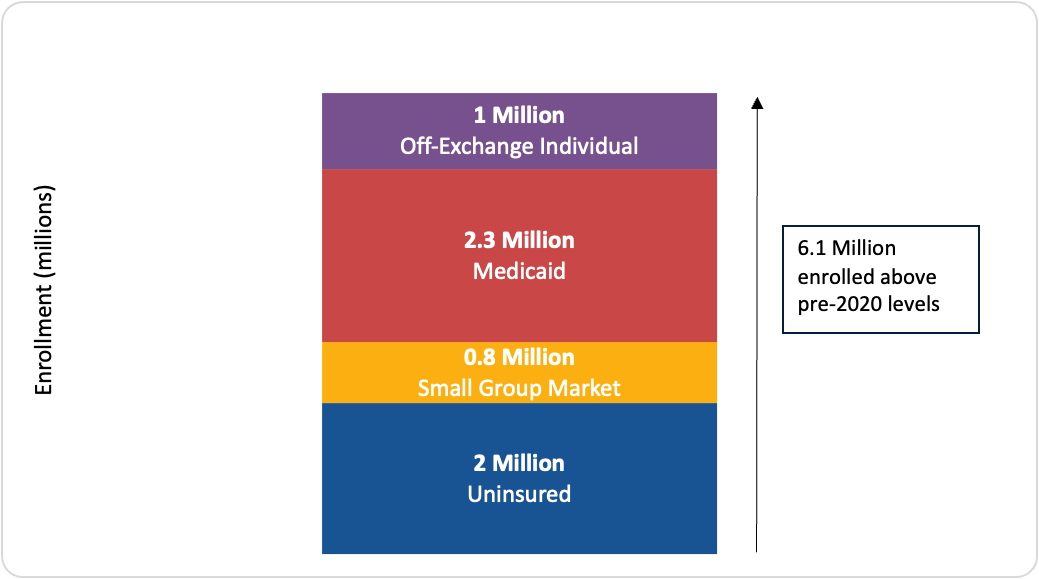

After accounting transitions into ACA Exchange coverage from alternative sources of coverage (Medicaid, off-ACA Exchange, small group ESI, uninsured), which we estimate is a combined 6.1 million Americans (labeled as other factors driving enrollment), enrollment is still 5.5 million above the 2019 effectuated enrollment average. We then subtract the 2.9 million that were removed after being found to be improperly or phantom enrolled and estimate that there remains 2.6 million potentially improper or fraudulent enrollees in 2026 (Figure 6). The difference between 2025 effectuated enrollment in February and 2025 effected enrollment in the same month is these 2.9 million improper or phantom enrollments removed. As a share of total enrollment (19.2 million) this represents 13.2 percent of enrollments that may be improper, fraudulent or phantom (2.6 million). This is high but not unheard of for federal programs, as an example, as recently as 2020, the improper payment rate in Medicaid was 21 percent. Due to bipartisan efforts, Medicaid improper payment rates have come down to 6 percent as of 202530. The improper payment rate for Medicare has hovered around 6- nearly 8 percent from 2020-2025 but has been as high as 12 percent in 201531.

Figure 6: Reductions in Improper, Fraudulent, and Phantom Enrollment from 2025 to 2026.

Note: CCIIO analysis of February effectuated enrollment, 2019, 2025, 2026.

In its analysis, CMS estimates the previous sources of coverage for this cohort of individuals that shifted into ACA Exchange plans come from the following sources.

Off-Exchange: CMS estimates about 1 million individuals were previously insured by ACA-compliant off-exchange plans. Off-exchange ACA-compliant individual enrollment fell from 3.5M in 2019 to 2.2M in 2024, a decline of 1.3M32,33. ARPA’s 2021 subsidy expansion accelerated the switching by making on-exchange coverage dominant for consumers without employer offers. We estimate roughly 1M of the 1.3M off-exchange decline migrated to on-exchange coverage by 2026, with the remainder returning to off-exchange coverage.

Medicaid: CMS estimates about 2 million were previously covered through the Medicaid program. The end of the COVID-19 public health emergency in April 2023 terminated the continuous-coverage requirement that had prevented Medicaid disenrollments for nearly three years. Approximately 4.8M individuals enrolled in ACA Exchange plans through the HealthCare.gov and state-based exchange Unwinding Special Enrollment Period (SEP) between April 2023 and November 30, 2024;34,35 this total encompasses HealthCare.gov states through the close of the SEP, as well as state-based exchanges, and is substantially larger than the publicly documented HealthCare.gov-only figure of approximately 2.4M through December 2023. Because the Unwinding SEP expired before the 2025 open-enrollment period, all Medicaid-unwinding enrollees still on exchange by late 2024 would subsequently re-enroll through standard open enrollment—either actively or through auto-reenrollment—making the Medicaid contribution essentially equal in both the open-enrollment count (2.4M) and the effectuated counts (2.3M). The small wedge reflects ordinary within-year attrition for any legitimate cohort.

Small Group Market: CMS estimates 800,000 were previously insured in the small employer (group) market. Small-group enrollment fell from 11.5M in 2020 to 9.0M in 2024, a decline of 2.5M36,37. The dominant driver is employers with 20 to 100 workers adopting self-funded or level-funded stop-loss arrangements, which are exempt from ACA community rating, essential health benefit mandates, and MLR requirements; firm-size growth into the large-group market is a secondary contributor. Most of the 2.5M decline reflects this employer reclassification—workers who remain covered under their employer but whose plans moved out of the fully-insured small-group market and therefore no longer appear in small-group enrollment counts; these workers do not enter the individual market. Of workers who actually lost employer-sponsored coverage and sought coverage elsewhere—through the individual market, a larger employer plan, Medicaid, or uninsured status—we attribute 0.8M to the ACA Exchange, a figure stable across all three endpoints because small-group employers’ coverage decisions are unrelated to enhanced subsidy expiration.

Uninsured: CMS estimates 2 million were previously uninsured. The non-elderly uninsured population fell from 28.9 million in 2019 to 25.4 million in 2023, a reduction of 3.5 million, concentrated among lower-income adults in the 100-to-400 percent FPL range where ARPA and IRA subsidies were most generous38. We attribute 2M of the 3.5M decline to ACA Exchange enrollment by 2026.

This yields a combined total of 6.1 million Americans that we estimate transitioned to ACA Exchange coverage from 2019-2026. Figure 7 shows this total and the which coverage source enrollees transitioned from.

Figure 7: Estimated Prior Coverage of Enrollment Above 2019 Levels.

Notes: CCIIO analysis of enrollment transitions across insurance states to ACA Exchange coverage from 2019-2026.

Additional Evidence Shows More Fraud and Improper Enrollments are Being Pulled Out

Media reports have focused narrowly on plan cancellations, a routine phenomenon that occurs primarily in the beginning of plan years as individuals are often auto-reenrolled into plans they may no longer want or need. Historically, 90-95 percent of enrollees who select an ACA Exchange plan during Open Enrollment ultimately effectuate coverage by paying their first premium32,39. These reports largely ignore the broader landscape, including that an estimated 2.9 million improperly enrolled individuals have been removed due to various program integrity measures. In addition to the about 1.5 million enrollees CMS previously removed from subsidies, we estimate another 1.4 million either ended coverage or were blocked from coverage due to recent policy changes. Various policies and metrics point to these improper and phantom enrollments being pulled out of the system from late 2025 to early 2026. This includes:

- The elimination of year-round enrollment for people with incomes between 100 to 150 percent FPL blocked these enrollments outside the open enrollment period.

- Already 27.8 percent of individuals in a plan where they pay no premiums whatsoever have canceled their plans through May 2026; the year-end share will almost assuredly be higher. The exact cause of each cancellation is unknown but may be attributable to individuals who became aware of being enrolled without their consent, having other sources of coverage, and possibly experiencing unexpected tax liability as a result of receiving premium subsidies they were not eligible for.

- Further, there is a significantly higher cancellation rate among those whose enrollment was agent- or broker-assisted compared to those that did not use an agent or broker. We estimate that more than 80 percent of cancellations are among enrollments that were assisted by an agent or broker. The disproportionate rate at which plan cancellations are being driven by those who were enrolled by agents and brokers further suggests that many plan cancellations are likely the result of the system shedding previously improper or fraudulent enrollments.

CONCLUSION

Preserving the fiscal and programmatic integrity of the ACA Exchanges is key to safeguarding taxpayer-funded resources for those that truly need them. The federal government paying brokers to enroll individuals without their knowledge is not. The Trump Administration continues to aggressively root out fraud, waste, abuse, and corruption by promulgating new regulations to improve program integrity, investigating suspected improper or fraudulent enrollment, and taking action against agents and brokers committing fraud. The Administration’s swift actions address these issues by preventing fraudulent and improper enrollment up front; remediating existing fraudulent and improper enrollments by cancelling them and/or ending their subsidy payments; and enforcing CMS regulations by terminating agents and brokers that violate them so they can’t continue committing fraud.

Most recently, after identifying over a million people who enrolled without a social security number, CMS shut down the ability for agents and brokers to get paid for assisting with enrollments through HealthCare.gov, started working with issuers to identify and remove unauthorized enrollments, and began implementing a framework to terminate agents and brokers responsible for unauthorized enrollments. By taking this bold action, the Trump Administration is cleaning up the fraudulent enrollments through ACA Exchanges which is both important to protect taxpayer dollars and to stabilize the individual market for consumers.

FOOTNOTES

[a] Alternatively, but less plausibly, enrollees with incomes between 100 and 150% of FPL are just healthier after 2021 than they were before, which is a strong assumption.

[b] These estimates are aligned with internal CCIIO Payment Policy and Financial Management Group (PPFMG) estimates.

REFERENCES

[1] United States, Congress. Inflation Reduction Act of 2022. Public Law 117-169, 117th Congress, 16 Aug. 2022.

[2] This issue brief defines phantom enrollment as individuals currently unaware of their ACA Exchange enrollment because they were auto-enrolled or enrolled by a broker while having no current-year contact with the program such as paying a premium or making a claim. Improper enrollees are receive subsidies but do not satisfy the statutory eligibility criteria.

[3] 45 C.F.R. §§ 155.220-155.221 (governing agents, brokers, web-brokers, and Enhanced Direct Enrollment entities on Exchanges). See also CMS, "Enhanced Direct Enrollment," https://www.cms.gov/marketplace-private-insurance/agents-brokers/direct….

[4] U.S. Government Accountability Office. "Patient Protection and Affordable Care Act: Preliminary Results from Ongoing Review Suggest Fraud Risks in the Advance Premium Tax Credit Persist." GAO-26-108742. December 2025.

[5] Knight V. "GOP Talking Point Holds ACA Is Haunted by 'Phantom' Enrollees, but the Devil's in the Data." KFF Health News. October 24, 2025.

[6] Gürel M. "The Impact of Brokers on ACA Exchange Growth." Risk Management and Insurance Review. 2024. See also Ritter Insurance Marketing, "How Much Can Agents Make Selling Under-65 Insurance?" 2025.

[7] Centers for Medicare & Medicaid Services. "CMS Actions to Protect Consumers and Strengthen Exchange Program Integrity." https://www.cms.gov/newsroom/fact-sheets/cms-actions-protect-consumers-….

[8] Government Accountability Office. Payment Integrity: Additional Coordination Is Needed for Assessing Risks in the Improper Payment Estimation Process for Advance Premium Tax Credits. GAO-23-105577, 9 Mar. 2023, https://www.gao.gov/products/gao-23-105577

[9] Government Accountability Office. Federal Health-Insurance Marketplace: Analysis of Plan Year 2015 Application, Enrollment, and Eligibility-Verification Process. GAO-18-169, 23 Jan. 2018, https://www.gao.gov/products/gao-18-169

[10] Government Accountability Office. State Health-Insurance Marketplaces: Three States Used Varied Data Sources for Eligibility and Had Few Indications of Potentially Improper Enrollments. GAO-17-694, 7 Sept. 2017, https://www.gao.gov/products/gao-17-694

[11] Government Accountability Office. Patient Protection and Affordable Care Act: Final Results of Undercover Testing of the Federal Marketplace and Selected State Marketplaces for Coverage Year 2015. GAO-16-792, 12 Sept. 2016, https://www.gao.gov/products/gao-16-792

[12] Government Accountability Office. Patient Protection and Affordable Care Act: CMS Should Act to Strengthen Enrollment Controls and Manage Fraud Risk. GAO-16-29, 24 Feb. 2016, https://www.gao.gov/products/gao-16-29

[13] Government Accountability Office. Patient Protection and Affordable Care Act: Preliminary Results of Undercover Testing of the Federal Marketplace and Selected State Marketplaces for Coverage Year 2015. GAO-16-159T, 22 Oct. 2015, https://www.gao.gov/products/gao-16-159t

[14] Stockley, Karen, et al. Premium Transparency in the Medicare Advantage Market: Implications for Premiums, Benefits, and Efficiency. National Bureau of Economic Research, June 2014, Working Paper no. 20208, https://doi.org/10.3386/w20208

[15] Centers for Medicare & Medicaid Services. “Patient Protection and Affordable Care Act; Updating Payment Parameters, Section 1332 Waiver Implementing Regulations, and Improving Health Insurance Markets for 2022 and Beyond Final Rule.” CMS Newsroom, 17 Sept. 2021, https://www.cms.gov/newsroom/fact-sheets/patient-protection-and-affordable-care-act-updating-payment-parameters-section-1332-waiver. Accessed 22 June 2026.

[16] 42 U.S.C. 18081 (c), (d), and (e); and 42 U.S.C. 18083 (c)..

[17] “Rising Complaints of Unauthorized Obamacare Plan-Switching and Sign-Ups Trigger Concern,” KFF Health News, April 8, 2024, https://kffhealthnews.org/news/article/aca-unauthorized-obamacare-plan-switching-concern/

[18] “Unauthorized sign-ups cast shadow on Obamacare’s record enrollment,” Washington Post, April 4, 2024, https://www.washingtonpost.com/politics/2024/04/04/unauthorized-sign-ups-cast-shadow-obamacares-record-enrollment/

[19] “Americans Clicked Ads to Get Free Cash. Their Health Insurance Changed Instead,” Wall Street Journal, September 13, 2024, https://www.wsj.com/health/healthcare/social-media-ads-health-insurance-scams-37d1ecfa?gaa_at=eafs&gaa_n=ASWzDAhqvMuucdjfzB_h2hV6pEwg31Tuml5fRjufggUT3-7YGyEHhxkyWOmD&gaa_ts=6892d030&gaa_sig=dNvkxk4HdWLhB-BiDhJBHKthFumze0nXulfEg_TruxC6NFgWDpch7kmf7xDFO4JU_pXLY_0cu2mnWGy-4124vw%3D%3D

[20] “The Great Obamacare Enrollment Fraud,” Paragon Health Institute, https://paragoninstitute.org/private-health/the-great-obamacare-enrollment-fraud/

[21] Centers for Medicare & Medicaid Services. 2024 Marketplace Open Enrollment Period Public Use Files.

[22] Decker, Sandra L., et al. “Health Service Use among the Previously Uninsured: Is Subsidized Health Insurance Enough?” Health Economics, vol. 21, no. 10, 2012, pp. 1155–1168.

[23] McGough, Matt, Krutika Amin, and Cynthia Cox. How Has Healthcare Utilization Changed Since the Pandemic? Peterson-KFF Health System Tracker, 24 Jan. 2023, https://www.healthsystemtracker.org/chart-collection/how-has-healthcare-utilization-changed-since-the-pandemic/. Accessed 25 June 2026.

[24] “CMS Finds 2.8 Million Americans Potentially Enrolled in Two or More Medicaid/ACA Exchange Plans,” Centers for Medicare and Medicaid Services, July 17, 2025, https://www.cms.gov/newsroom/press-releases/cms-finds-28-million-americans-potentially-enrolled-two-or-more-medicaid/aca-exchange-plans

[25] “Victims of Biden’s Enrollment-At-Any-Cost Exchange Strategy,” Paragon Health Institute, July 18, 2025, https://paragoninstitute.org/paragon-prognosis/victims-of-bidens-enrollment-at-any-cost-exchange-strategy/

[26] Centers for Medicare & Medicaid Services. 2025 Marketplace Integrity and Affordability Final Rule. Centers for Medicare & Medicaid Services, 20 June 2025, https://www.cms.gov/newsroom/fact-sheets/2025-marketplace-integrity-and-affordability-final-rule

[27] City of Columbus et al. v. Kennedy et al. United States District Court for the District of Maryland, No. 1:25-cv-02114-BAH, Memorandum Opinion, 22 Aug. 2025.

[28] Centers for Medicare & Medicaid Services. "CMS Takes Aim to Reduce Improper Enrollments and Promote More Affordable Health Insurance Marketplaces for Millions of Consumers." Centers for Medicare & Medicaid Services, 10 Mar. 2025, https://www.cms.gov/newsroom/press-releases/cms-takes-aim-reduce-improper-enrollments-and-promote-more-affordable-health-insurance-marketplaces

[29] Centers for Medicare & Medicaid Services. CMS Actions to Protect Consumers and Strengthen Exchange Program Integrity. Centers for Medicare & Medicaid Services, 28 Jan. 2026, https://www.cms.gov/newsroom/fact-sheets/cms-actions-protect-consumers-strengthen-exchange-program-integrity

[30] Centers for Medicare & Medicaid Services. PERM Error Rate Findings and Reports. U.S. Department of Health and Human Services, 20 Jan. 2026, https://www.cms.gov/data-research/monitoring-programs/improper-payment-measurement-programs/payment-error-rate-measurement-perm/perm-error-rate-findings-and-reports. Accessed 26 June 2026.

[31] Centers for Medicare & Medicaid Services. "Improper Payment Rates and Additional Data." CMS.gov, U.S. Department of Health and Human Services, 16 Jan. 2026, https://www.cms.gov/data-research/monitoring-programs/improper-payment-measurement-programs/comprehensive-error-rate-testing-cert/improper-payment-rates-and-additional-data. Accessed 26 June 2026.

[32] Mark Farrah Associates. (2019). Current trends in individual segment enrollment. https://www.markfarrah.com/mfa-briefs/current-trends-in-individual-segm…

[33] Fehr, R., Cox, C., & Levitt, L. (2023). Recent trends in the individual insurance market. KFF. https://www.kff.org/private-insurance/issue-brief/recent-trends-in-the-…

[34] KFF. (2024). Medicaid enrollment and unwinding tracker. KFF. https://www.kff.org/medicaid/issue-brief/medicaid-enrollment-and-unwind…

[35] CMS. (2024). Marketplace special enrollment period data. Centers for Medicare & Medicaid Services. https://www.cms.gov/data-research/statistics-trends-and-reports/marketp…

[36] Mark Farrah Associates. (2025). An analysis of profitability for the individual and small group health insurance markets in 2024. https://www.markfarrah.com/mfa-briefs/an-analysis-of-profitability-for-…

[37] KFF. (2024). 2024 employer health benefits survey. KFF. https://www.kff.org/health-costs/report/ehbs-2024/

[38] Keisler-Starkey, K., & Bunch, L. N. (2024). Health insurance coverage in the United States: 2023 (Report P60-284). U.S. Census Bureau. https://www.census.gov/library/publications/2024/demo/p60-284.html

[39] Lo, Justin, Jared Ortaliza, Emma Wager, Matt McGough, and Cynthia Cox. ACA Exchange Enrollment Is Down in 2026—But All of the Data Isn't in Yet. KFF, 5 Feb. 2026, https://www.kff.org/affordable-care-act/aca-marketplace-enrollment-is-d…

*This content is in the process of Section 508 review. If you need immediate assistance accessing this content, please submit a request to Scott Smith, scott.smith@hhs.gov. Content will be updated pending the outcome of the Section 508 review